Protect yourself against the financial risks of critical illness this Movember

Peter Dempsey, deputy CEO of ASISA.

More than 100 000 South Africans are diagnosed with cancer every year, and South African men have a one in eight chance of being diagnosed with cancer in their lifetime, according to National Cancer Registry statistics for 2010.

Peter Dempsey, deputy CEO of the Association for Savings and Investments South Africa (ASISA), states that it is therefore vital to not only take responsibility for your health with a full annual check-up, but to also protect yourself and your family against the financial consequences of being diagnosed with a critical illness such as cancer or heart disease.

With October’s Breast Cancer Awareness just past and Movember upon us, Dempsey says that now is the perfect time to initiate proactive steps to safeguard your family’s financial well-being with comprehensive life and critical illness cover.

“Beyond the physical and emotional toll of suffering a critical illness, there is also the enormous financial strain that is often placed on families. A severe illness may result in the breadwinner not being able to work. In addition, there may be travel expenses, costly treatments not covered by medical aid cover, or having to pay for a carer,” he says.

“Critical illness or dread disease products are therefore designed to pay out a benefit when you are diagnosed with a serious illness or suffer a traumatic medical event such as a stroke or heart attack which could result in financial hardship.”

He notes that while many South Africans still consider insurance a grudge purchase, in the year to the end of June 2016 life insurers honoured the overwhelming majority of claims made against underwritten policies, paying some R36.5 billion to beneficiaries of life, disability, income protection or critical illness cover.

“These benefit payments helped protect many families from financial hardship following the death, disability or critical illness of a breadwinner.”

The role of critical illness cover

Dempsey emphasises that income protection and disability cover are not a replacement for insurance in case of critical illness.

“You may be technically able to continue working after an event such as a minor heart attack, which means that you may not qualify for a pay out from your disability or income protection cover,” he explains.

“However, if you needed to make some lifestyle changes and scale back on your workload to reduce your stress levels, the payout from your critical illness cover would help plug the gap in your income.”

While the range of illnesses covered by critical illness products differs from insurer to insurer, the ‘big four’ conditions most commonly included are heart attacks, cancer, strokes and coronary artery by-pass grafts for heart disease.

Dempsey states that these four conditions account for more than half of all critical illness events, but that you should also take your individual history and circumstances into account when choosing your policy.

“Some policies offer benefits for conditions ranging from Alzheimer’s to Tuberculosis and major burns for example,” he says.

He notes that some companies may also offer a cover reinstatement option for other illnesses after you have made a claim. This means that if, for example, you suffer a heart attack and are later diagnosed with cancer, you may claim from your insurance again, he explains.

Types of critical illness products

Dempsey states that there are two broad categories of critical illness cover, namely severity-based and diagnosis-based.

Severity-based cover tends to be cheaper, because these policies pay benefits based on the level of severity of your medical condition or event. This means that the amount you would receive could differ, for instance, if you suffered a minor stroke versus a major stroke.

“By comparison, diagnosis-based cover will pay the full benefit provided certain medical criteria are met. This type of insurance therefore tends to be more expensive,” explains Dempsey.

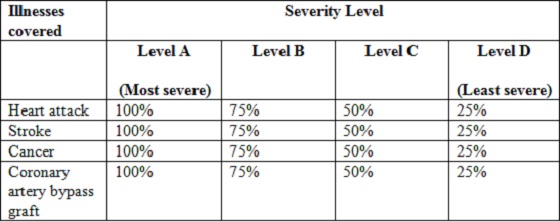

He notes that ASISA introduced a standardised critical illness disclosure grid in 2009 that will help you compare benefits for the aforementioned ‘big four’ medical conditions across different policies, based on standardised definitions. ASISA member companies include this grid in your policy quotation with a list of illnesses addressed by the policy.

The grid sets out the percentage of your cover that your insurer would pay in each circumstance according to the level of severity of your illness as demonstrated below:

Payouts as a percentage of the cover amount:

Dempsey cautions, however, that critical illness products involve numerous other complexities, technicalities and medical concepts that can be difficult to understand.

“The wisest course of action would therefore be to approach a financial adviser for assistance in selecting the best type of insurance for your needs according to your individual affordability. You should also try to make time for annual check-ups and the necessary tests to ensure that any issues are detected as early as possible. ”

“Times are tough, but the value of seeking advice and ensuring that you are adequately protected against death, disability and critical illness will become immediately apparent should the unexpected happen.”