Living annuity drawdown rates show marginal increase in 2016

Taryn Hirsch, senior policy advisor at ASISA.

Living annuity policyholders withdrew on average 6.62% of their capital as income in 2016, which represents a marginal increase in the 6.44% living annuity drawdown rate recorded for 2015.

According to the 2016 Living Annuities Survey compiled by the Association for Savings and Investment South Africa (ASISA), South Africans had R333.2 billion of their retirement savings invested in 380 186 living annuities. In 2015, there were 410 898 living annuities with assets of R331.6 billion.

Commenting on the 2016 Living Annuities Survey, Taryn Hirsch, senior policy advisor at ASISA, says the small increase in the drawdown rate came as a pleasant surprise given the steep rise in the cost of living in South Africa in recent years.

“While we would have preferred to see the drawdown rate continue the small yet steady downward trend of the past five years, we have to accept that many pensioners are finding it increasingly difficult to maintain their standard of living without adjusting their drawdown rates upward.

“We need to take into consideration that inflation came in at 6.6% for 2016 and the JSE All Share Index returned only 2.6%. Under those circumstances the small increase is understandable and pensioners and their advisers need to be commended for tightening the proverbial belt rather than increasing their drawdown rates substantially.”

Capital erosion

Hirsch says that while living annuity policyholders are required to draw a regular income of between 2.5% and 17.5% of the value of their living annuity assets, the majority of pensioners risk eroding their capital by drawing more than 5% as income.

“When the percentage of income drawn exceeds the real returns of the investment portfolio supporting the living annuity, the capital base will be eroded over time,” explains Hirsch.

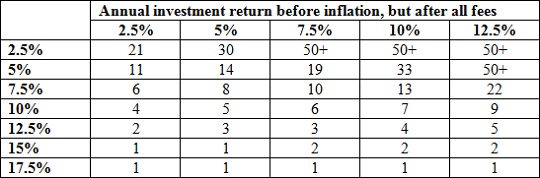

For this reason the ASISA Standard on Living Annuities, which came into effect in 2010, requires member companies to include the following table in client communication when reminding living annuity policyholders to select their annual drawdown rates:

Years before your income will start to reduce

It is important to note that the table above assumes that the income drawdown rate is adjusted over time to maintain a real income by allowing for inflation of 6% a year. Once the number of years in the table above has been reached, the pensioner’s income will diminish rapidly in the subsequent years.

The ASISA Standard on Living Annuities, also requires member companies to provide a living annuity status report to ASISA at the end of each year. The survey makes it possible for ASISA to monitor the level of income drawn by policyholders from their retirement capital as well as the general asset composition of living annuity investment portfolios.

When ASISA started collecting consolidated statistics on South Africa’s living annuity book in 2011 the average drawdown level was 6.99%.

Average living annuity drawdown levels* over 6 Years

![]()

* The average income drawdown level is weighted by fund size (the total value of the drawdowns against the total value of the living annuity book).

Prudential guidelines

Unlike retirement funds, living annuities are not legally required to adhere to prudential investment guidelines as detailed in Regulation 28 of the Pension Funds Act. However, says Hirsch, ASISA recommends that policyholders take these guidelines into consideration when compiling their living annuity portfolios.

Last year 31.03% of living annuity policies did not apply the prudential investment guidelines compared to 33.59% in 2015.

In terms of the prudential guidelines, exposure to the various asset classes should not exceed the following:

• equity investments – 75%

• non-government debt instruments – 50%

• offshore investments – 25%

• property investments – 25%

• hedge funds, private equity funds and other assets – 15%

• commodities like gold – 10%

What is a living annuity?

A living annuity is a special type of compulsory purchase annuity that does not guarantee a regular income. The income (or annuity amount) is dependent on the performance of the underlying investments. Living annuities allow clients to select an income level that ranges between a pre-defined minimum and maximum level.

Three key factors determine how long the capital will be able to produce a regular income:

• The level of income selected;

• Performance of selected investments; and

• The lifespan of the annuitant