Life insurers report a spike in fraudulent death claims for 2017

South African life insurers foiled a total of 5 026 irregular claims to a value of R1.13 billion in 2017.

The Association for Savings and Investment South Africa (ASISA) this week released the 2017 consolidated statistics of fraudulent and dishonest claims, which show that while the total number of thwarted fraudulent and dishonest claims across different types of long-term insurance products was much lower in 2017 than in 2016 when 13 488 claims (mostly funeral claims) proved to be irregular, the value was almost the same. In 2016 fraudulent and dishonest claims worth R1.03 billion were detected.

Donovan Herman, convenor of the ASISA Claims Standing Committee, points out that life insurers are under constant pressure to adapt their detection methods as fraud attempts become more sophisticated due to fast evolving technology.

He says while life insurers are frequently accused of trying to find ways of getting out of paying claims, the numbers tell a different story. While claims worth R1.13 billion were found to be irregular and therefore not paid in 2017, South African life insurers made benefit payments of R469 billion to policyholders and beneficiaries in the same year. Of this amount, more than R60 billion was paid to individuals who had experienced either death or disability in their family circle – an increase of almost R5 billion from 2016.

“The reality is that as the custodians of a significant portion of South Africa’s savings pool, life insurers are obliged to protect the integrity of this savings pool and the interests of honest policyholders by preventing fraud and dishonesty.

“If we left fraud and dishonesty to spiral out of control, honest policyholders would end up footing the bill through higher premiums driven by untenable claims rates.”

Below follows a summary of irregular claims detected for different types of long-term insurance cover.

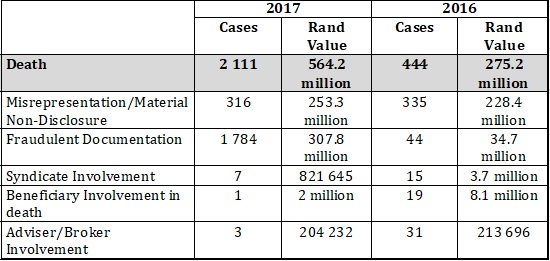

Death claims

A total of 2 111 death claims worth R564.2 million was declined in 2017 due to fraud and dishonesty compared to 444 death claims worth R275.2 million in 2016.

In the majority of death claims (1 784) rejected in 2017, insurers detected that fraudulent documentation had been submitted. A further 316 claims were declined due to misrepresentation and/or material non-disclosure.

Misrepresentation occurs when a policyholder deliberately provides misleading information to a life insurer, while material non-disclosure refers to the failure of policyholders to disclose important information about a medical condition or lifestyle.

Since the person applying for insurance knows more about the risk to be insured than the insurer, the law compels applicants to honestly disclose all information likely to influence the judgment of the insurer when determining appropriate policy terms and premiums. Information generally regarded as material include medical history, state of health, family history, and life style. Only when all the facts are disclosed honestly by the applicant is the insurer able to set premiums that are appropriate for a certain level of risk, thereby ensuring that every person pays a fair premium without subsidising someone less healthy.

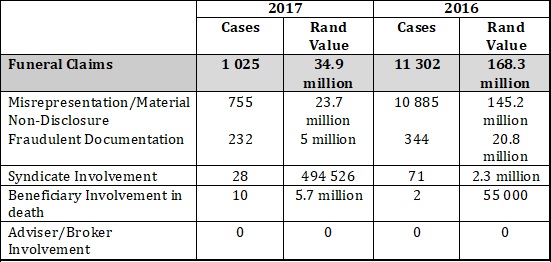

Funeral claims

A total of 1 025 funeral claims worth R34.9 million was rejected in 2017, mainly due to misrepresentation and material non-disclosure, as well as fraud. In 2016, there were 11 302 irregular funeral claims worth R168.3 million.

Herman says funeral policies are designed to pay out quickly and without hassle when an insured family member dies. They also do not require blood tests and medical examinations. “This can tempt people to take out funeral cover on people that do not exist or to buy funeral cover only once they have developed a serious illness and are expecting to die as a result.”

Life insurers have reported a number of cases where funeral cover was taken out on the lives of people under the pretence that they were family members of the policyholder, when in fact they were either colleagues, fellow church members or even fictional people.

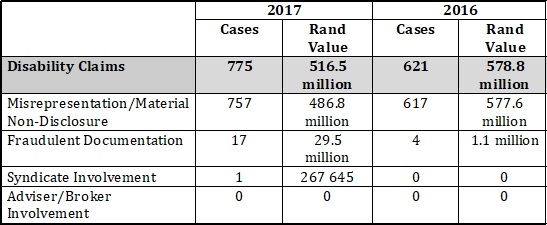

Disability claims

Misrepresentation and material non-disclosure by policyholders was by far the biggest reason for disability claims worth R516.5 million being declined in 2017. Out of the 775 claims not paid, 757 were rejected due to misrepresentation or material non-disclosure. In 2016, some 621 claims worth R578.8 million were rejected.

Herman says over the past two years the life industry noticed a significant increase in legitimate claims against individual disability policies. “Since disability claims tend to increase when the economy is under strain, we are not surprised that dishonest claims also increased significantly.”

He says policyholders are often tempted to not disclose existing health conditions with the aim of securing lower premiums. “This is very short sighted since the life insurer is likely to uncover deliberate attempts to hide material information, which will lead to claims being declined.”

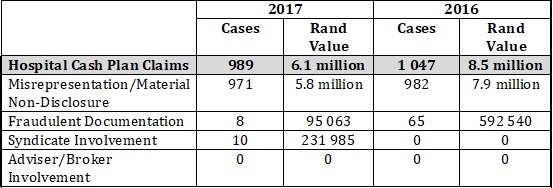

Hospital cash plans

Strict measures introduced by life insurers a couple of years ago to curb the abuse of hospital cash plans continued to pay off as fraudulent and dishonest claims against hospital cash plans showed a further decline in 2017. A total of 989 claims worth R6.1 million was declined compared to 2016 when 1 047 claims worth R8.5 million were rejected.

Herman says hospital cash plans are easy to understand products designed to help consumers cope with unexpected expenses as a result of being admitted to hospital. Unfortunately, he adds, the simplicity of these products leaves them wide open to abuse.

This forced life insurers to implement tough measures to ensure the financial viability of these products.

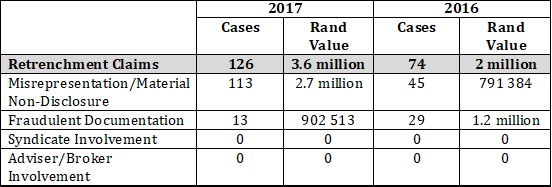

Retrenchment benefit claims

Dishonest and fraudulent retrenchment claims increased from 74 in 2016 to 126 in 2017. Life insurers declined 113 claims due to misrepresentation and non-disclosure and 13 due to fraud.

The total value of these claims amounted to R3.6 million in 2017, compared to R2 million in 2016.

Most dishonest provinces

Herman reports that 31% of all fraudulent and dishonest claims were detected in KZN, followed by the Eastern Cape with 22.3% and Gauteng with 20.5%.

The Western Cape was responsible for 6.7% of claims declined and the Freestate for 5.1%. Other provinces were responsible for 5% or less.