Life insurers pay claims and benefits worth R287.1 billion in the first half of 2023

Beneficiaries and policyholders received R287.1 billion in claims and benefits from South African life insurers in the first half of 2023. The payments would have reached these beneficiaries and policyholders at a time of great need – following a tragic life event like death or disability or a life stage change like retirement.

The long-term insurance statistics released by the Association for Savings and Investment South Africa (ASISA) for the first six months of this year show that despite the significant pay-outs, life insurers remain well-capitalised and in a solid position to honour the long-term contractual promises made to customers.

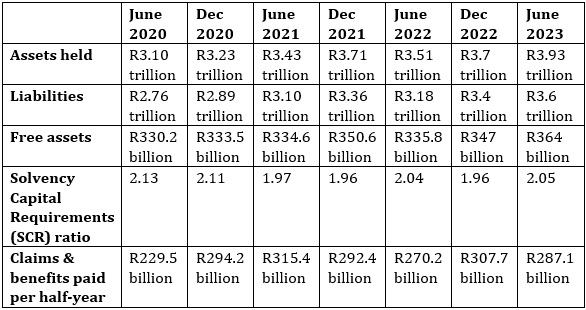

According to Gareth Friedlander, a member of the ASISA Life and Risk Board Committee, the life insurance industry held assets of R3.93 trillion at the end of June 2023, while liabilities amounted to R3.6 trillion. This left the industry with free assets of R364 billion, more than double the reserve buffer required by the Solvency Capital Requirements (SCR).

Healthy reserves are a critical indicator of the health of the long-term insurance industry, providing policyholders with the peace of mind that claims and policy benefits can be paid even in times of extreme market turmoil and/or unusually high claims.

“Life insurers displayed significant resilience over the past three years in an unprecedented operating environment marked by the effects of a global pandemic, a struggling economy and consumers under severe financial pressure,” says Friedlander.

He adds that assets held by South African life insurers have shown steady growth over the past three years, from R3.10 trillion at the end of June 2020 to R3.93 trillion at the end of June 2023.

The life industry in number

Recurring premium business remains flat

The ASISA long-term insurance statistics show that close to 5 million new recurring premium risk policies (life policies, funeral policies, credit life policies, disability policies, severe illness policies and income protection policies) were sold between January and June 2023. At the same time, however, 4.3 million risk policies were lapsed. A lapse occurs when the policyholder stops paying premiums for a risk policy with no accumulated fund value.

Friedlander says the lapse rate is concerning since 4.3 million policyholders and their beneficiaries are now living either without risk cover or with reduced cover.

He acknowledges that a high lapse rate is a reflection of the country’s economic situation and the severe financial strain faced by many consumers on the back of rising interest rates.

In the first half of this year, the repo rate increased twice by 0.5%, taking it to a 14-year high of 8.25% and placing an additional burden on consumers servicing debt like home loans and car repayments. In addition, several fuel price increases contributed towards a rise in living costs in South Africa, where 32.9% of the population is unemployed, according to the Quarterly Labour Force Survey (QLFS) for the first quarter of 2023.

Friedlander also notes that surrenders of recurring savings policies (endowments and retirement annuities) exceeded the sales of these policies in the first half of 2023. While 284 647 policies were sold, 313 318 were surrendered. A surrender of a policy occurs when the policyholder stops paying premiums and withdraws the fund value before maturity.

He says this is unsurprising since consumers are more likely to surrender their savings policies during tough times to cope with financial hardship.

At the end of June 2023, there were 34.2 million recurring premium risk policies in force and 203 578 single premium risk policies. Recurring premium savings policies amounted to 5.3 million as at 30 June 2023, and there were 2.4 million single premium savings policies.

Message to consumers

Friedlander says without the buffer provided by risk cover, a tragic life event like death or disability can plunge a household already struggling financially into complete ruin. He urges consumers to consider all other options before giving up their risk cover.

“The COVID pandemic highlighted the importance of having risk cover in place like few other events in the history of South Africa. Many life insurers paid a record number of claims, and while these payouts cannot replace loved ones, they can prevent further trauma caused by the financial impact of the loss of a breadwinner.”

According to the 2022 ASISA Life and Disability Insurance Gap Study, the average South African income earner had a life insurance shortfall of at least R1 million and a disability cover gap of around R1.4 million at the end of 2021.

The study, conducted every three years, shows that South Africa’s 14.3 million income earners had life and disability insurance to cover only 45% of the total insurance needs of their households. The average South African household supported by at least one income earner would, therefore, be forced to cut living expenses should the earner die or become disabled, and no other source of income can be found.

Friedlander encourages policyholders struggling to make ends meet to discuss options with their financial advisers before letting go of their risk cover. “A financial adviser can help you by taking a holistic view of your financial situation and helping you find sustainable solutions that are not driven by emotions.”