Life insurers block dishonest and fraudulent claims worth more than R1 billion

South African life insurers reported significant increases in dishonest and fraudulent long-term insurance claims for 2016.

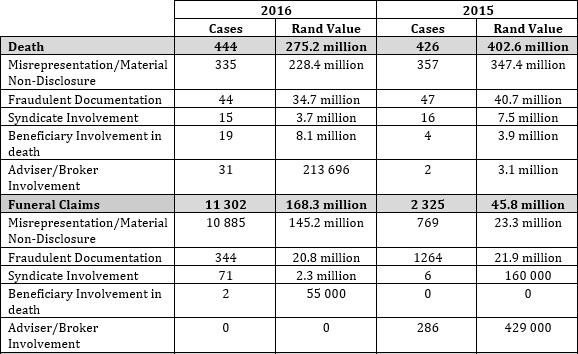

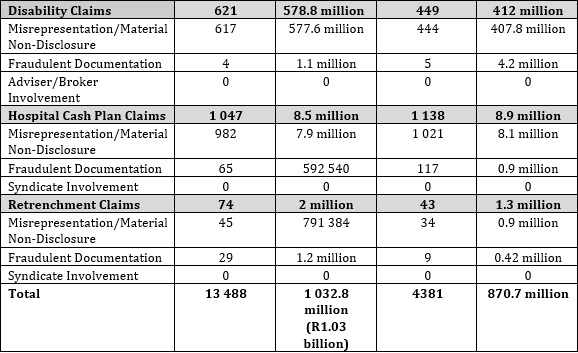

Claims fraud statistics released this week by the Association for Savings and Investment South Africa (ASISA) show that the number of irregular claims detected in 2016 more than tripled to 13 488 from 4 381 claims in 2015. The value of the thwarted fraudulent and dishonest claims jumped from R870.7 million in 2015 to R1.03 billion in 2016.

Donovan Herman, convenor of the ASISA Claims Standing Committee, points out that for the same period the industry paid more than R38 billion to honest individuals who had experienced either death or disability in their family circle.

“Life insurers act as custodians of a significant portion of South Africa’s savings pool, injecting much needed funds back into the economy with the payment of benefits. Through the prevention of fraud and dishonesty, insurers maintain the integrity of this savings pool for the benefit of honest policyholders.”

Herman says while the increase in dishonest and fraudulent claims is concerning, it is not surprising.

“Policyholders are feeling the effects of an economy under pressure and as a result some are tempted into submitting dishonest claims, committing fraud or colluding with syndicates,” he says.

He adds that ASISA member companies continue implementing improved measures to detect instances of fraud and dishonesty, which is paying off through a much higher detection rate.

Funeral claims

The biggest increase in irregular claims was reported for funeral policies. An unprecedented 11 302 claims worth R168.3 million were foiled in 2016, mainly due to misrepresentation and material non-disclosure. In 2015, there were 2 325 irregular funeral claims worth R45.8 million.

Misrepresentation occurs when a policyholder deliberately provides misleading information to a life insurer. Material non-disclosure refers to the failure of policyholders to disclose important information about a medical condition or lifestyle.

Herman says funeral policies are designed to pay out quickly and without hassle when an insured family member dies. They also do not require blood tests and medical examinations. “This can tempt people to take out funeral cover on people that do not exist or to buy funeral cover only once they have developed a serious illness and are expecting to die as a result.”

Life insurers have reported a number of cases where funeral cover was taken out on the lives of people by policyholders claiming that they were family members, when in fact they were either colleagues, fellow church members or even fictional people.

In one such case, a policyholder included her minor child on her funeral cover. When she submitted a claim for the deceased child, the life company became suspicious when contradictions were noticed in the supporting documents.

Further investigation revealed that nobody had actually seen or handled the body. The traditional leader, who had signed the form, admitted that he had completed the form in good faith and that he had not seen the body of the child.

It was also found that there were no Home Affairs records confirming the birth of the child or any clinic records. A case of fraud has been opened against the policyholder.

Disability claims

Misrepresentation and material non-disclosure by policyholders resulted in 617 disability claims worth R577.6 million being declined in 2016, compared to 444 claims worth R407.8 million in 2015.

Herman says starting from July 2016 to June 2017 the life industry also noticed a significant increase of 21% in legitimate claims against individual disability policies.

“Considering that an unusually high increase in legitimate disability claims is usually indicative of consumers under severe financial strain, we are not surprised that dishonest claims also increased so significantly.”

“Some policyholders deliberately do not disclose existing health conditions with the aim of securing lower premiums. This is very short sighted since the life insurer is likely to uncover deliberate attempts to hide material information, which will lead to claims being declined.”

Death claims

A total of 444 death claims were declined in 2016 due to dishonesty and fraud compared to 426 in 2015. However, the value of these claims was much lower in 2016 at R275.2 million, compared to R402.6 million in 2015.

In the same period life insurers honoured 99.3% of claims against fully underwritten life policies to a record value of R13.1 billion. Fully underwritten life policies are only issued if the policyholder has completed a full underwriting process, which may involve a comprehensive assessment of the life insured’s medical history.

Herman says this demonstrates the value of being upfront with your insurer and paying the appropriate premium rather than risking losing the value of your policy.

Hospital cash plans

A total of 1 047 fraudulent and dishonest claims against hospital cash plans worth R8.5 million were declined in 2016. This represents a slight decline from 2015, when 1 138 claims worth R8.9 million were rejected.

Hospital cash plans pay policyholders a daily cash benefit for each day spent in hospital. This amount is paid irrespective of medical aid payments or sick leave benefits available to the person hospitalised.

Retrenchment benefit claims

Dishonest and fraudulent retrenchment claims increased from 43 in 2015 to 74 in 2016. Life insurers declined 45 claims due to misrepresentation and non-disclosure and 29 due to fraud.

The total value of these claims amounted to R2 million in 2016, compared to R1.3 million in 2015.

Most dishonest provinces

Herman reports that 36.2% of all fraudulent and dishonest claims were detected in the Eastern Cape, followed by KZN with 29.5%.

Gauteng was responsible for 13.2% of claims declined and the Western Cape for 5.2%. Other provinces were each responsible for 5% or less.

Fraudulent and dishonest policy claims statistics for 2016, compared to 2015

Figures have been rounded