Hospital cash plans under attack

Peter Dempsey, deputy CEO of ASISA.

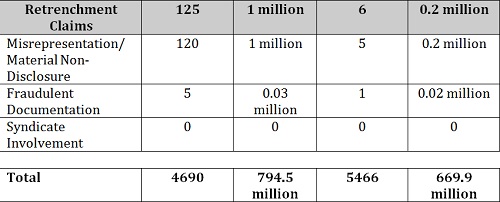

The South African life insurance industry reported a reduction in the number of fraudulent and dishonest long-term insurance claims uncovered in 2013 compared to 2012. The value of these claims, however, increased substantially from R669.9 million in 2012 to R794.5 million in 2013.

Claims fraud statistics released by the Association for Savings and Investment South Africa (ASISA) this week show that 4 690 fraudulent and dishonest death, funeral, disability, health and hospital as well as retrenchment claims were detected and prevented in 2013, compared to 5 466 in 2012.

Peter Dempsey, deputy CEO of ASISA, points out that had these claims gone undetected, the industry would have lost R794.5 million to dishonest policyholders and criminals in 2013.

Dempsey explains that if left unchecked, fraudulent and dishonest claims would over time substantially increase the claims experience of life companies and ultimately force companies to recover these losses from customers through increased premiums.

He points out, however, that by far the majority of claims submitted to life companies are honest and legitimate and therefore honoured. The beneficiaries of individual policyholders who had death and disability cover in place received benefit payments worth R26.7 billion from the life insurance industry in 2013.

“Life companies paid 98.9% of all claims made against fully underwritten life policies in 2013. Only 1.1% of death benefit claims were declined.”

According to Dempsey, death and funeral policies and hospital cash plans attracted most of the dishonest and fraudulent activity in 2013.

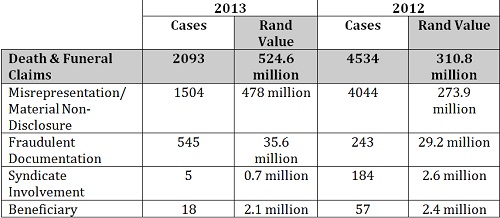

Death and funeral claims

The total number of irregular death and funeral claims detected in 2013 was less than half the number thwarted in 2012. In 2013 there were 2 093 claims, compared to 4 534 in 2012. However, the value of these claims was substantially higher in 2013 at R524.6 million compared to R310.8 million in 2012.

Dempsey points out that the majority of irregular death and funeral claims detected in 2013 involved dishonesty through misrepresentation and material non-disclosure rather than the criminal intent of fraud. In total 1 504 claims worth R478 million were found to have involved either misrepresentation or material non-disclosure.

Misrepresentation occurs when a policyholder deliberately provides misleading information to a life insurer. Material non-disclosure refers to the failure of policyholders to disclose important information about a medical condition or life style.

In 545 cases fraudulent documentation was submitted, in 18 cases the beneficiaries were involved in submitting fraudulent death claims, in 21 cases the intermediary was found to have been dishonest and in only five cases syndicates were involved.

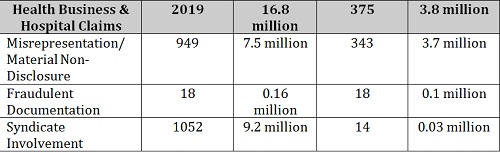

Hospital cash plans

Hospital cash plans were hit particularly hard in 2013. For the first time the number of dishonest and fraudulent claims against these plans almost equalled those against death and funeral cover, which in the past always attracted the highest level of dishonesty and criminal activity.

Dempsey points out that syndicate involvement was behind the majority of fraudulent hospital cash plan claims in 2013. “Our members detected a total of 2 019 dishonest and fraudulent hospital cash plan claims to a value of R16.8 million, of which 1 052 were cases of fraud perpetrated by syndicates to a value of R9.2 million. In 2012 there were only 14 cases involving syndicates.”

Dempsey described as good news the fact that ASISA members detected such a high number of fraudulent claims in the hospital cash plan space. “The reality is that it is very difficult for individual members to defraud their hospital cash plan without help from doctors and hospital staff. Through sharing of information and working closer with medical aid schemes, insurers are identifying syndicates consisting of doctors and hospital staff and are increasingly clamping down on such claims.”

According to Dempsey the abuse of hospital cash plans is a major concern for insurers. “Insurers have taken a zero tolerance approach to claims involving any kind of fraud, which may result in a criminal investigation and even prison.”

Hospital cash plans pay policyholders a daily cash benefit for each day spent in hospital. This amount is paid irrespective of medical aid payments or sick leave available to the person hospitalised.

Misrepresentation and material non-disclosure resulted in 949 claims against hospital cash plans being rejected to a value of R7.5 million. Fraudulent documentation was detected in 18 claims worth R156 442.

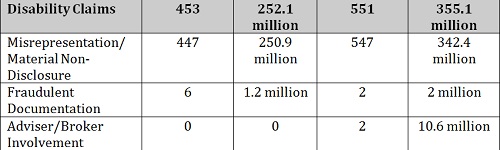

Disability claims

The majority of disability claims were rejected due to misrepresentation and material non-disclosure rather than fraud. A total of 447 claims worth R251 million were found to be dishonest. Only six fraudulent claims worth R1.2 million were detected.

Retrenchment benefit claims

Dempsey says in the past the industry recorded very few dishonest or fraudulent retrenchment benefit claims. This changed in 2013 with 125 retrenchment benefit claims worth just over R1 million rejected to due to misrepresentation and material non-disclosure as well as fraud. In 2012 there were 6 cases.

“This is a sure sign that consumers are taking strain and clutching at straws when their jobs are on the line,” says Dempsey. He warns, however, that dishonesty and fraud should never be the last resort as the consequences are likely to be severe.”

Why misrepresentation and non-disclosure is short-sighted

Policyholders are legally obliged to honestly disclose all information likely to influence the judgment of the insurer when determining appropriate policy terms and premiums. Information generally regarded as material by a life insurer includes medical history, state of health, family medical history, life style and financial status.

Dempsey says there will always be policyholders who will try to keep their premiums to a minimum by not disclosing all risks and get as much as possible from their cover without having to pay for it.

“This is usually not a wise decision. It is much better to be completely honest and pay the appropriate premium than to run the risk of having a claim declined when you die or become disabled.”

According to Dempsey the majority of dishonest and fraudulent claims are detected. “Dishonest policyholders risk losing their cover and fraudsters may end up doing jail time.”

Fraudulent and dishonest policy claims statistics for 2013, compared to 2012

Figures have been rounded up.