Christmas gifts that will never end up in a thrift shop

Peter Dempsey, Deputy CEO of ASISA.

Retailers have started enticing shoppers to splurge on Christmas gifts, but the Association for Savings and Investment South Africa (ASISA) is hoping to convince consumers to rather gift financial products designed to grow in value over time.

Peter Dempsey, Deputy CEO of ASISA, says that the best gifts you can give your loved ones are saving and investment products that will sustain them for years to come.

“As the saying goes – all that glitters isn’t gold,” says Dempsey. “Instead of superficial spending on presents, why not consider a financial gift that will prove far more valuable to your loved ones down the road?”

He discusses some examples of financial products that families could consider as gifts for the upcoming festive season. If you are inclined to spend on a gift that will definitely not end up in a thrift shop a couple of months from now, make an appointment with a trusted financial adviser who will help you choose products best suited to your loved ones’ long-term needs.

Young children

Parents looking to give their children a significant financial jumpstart could start a tax free savings or investment account in their child’s name, says Dempsey.

Tax free savings accounts were introduced in March this year to encourage South Africans to become long-term savers. Individuals may invest up to R30 000 a year and R500 000 in a lifetime, free of capital gains, income and dividends tax. Any contributions above these amounts are punitively taxed.

While you may withdraw money from these accounts, you cannot replace these amounts as they will still be viewed as contributions to your lifetime allowance. Dempsey points out that tax free savings accounts are thus ideally a long-term investment.

“Arguably your children wouldn’t be paying tax anyway, but by investing in a tax free savings product, your children will see the benefit of the compounding on this investment later in their life, free of tax,” explains Dempsey.

“By allowing this investment to grow over time, your children could receive a significant amount of money to put towards tertiary education, a property or even their retirement,” he says.

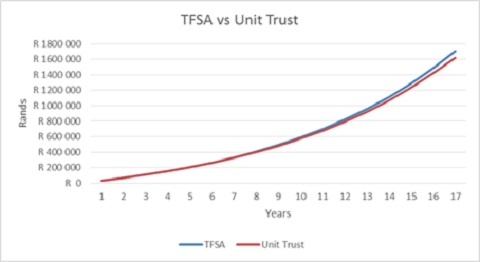

Depending on your means you can invest up to R2 500 a month (or R30 000 a year) into a tax free account for each child. If you do contribute R2 500 a month you would reach the lifetime contribution limit of R500 000 in 16.5 years.

Assuming a 13% net return on this investment, Dempsey explains that your child would then have a tax free lump sum of R1.7 million. If the same investment, also earning a 13% net return, was made into a taxable investment product, it would grow to R1.62 million after tax – R80 000 less. This amount would then be subject to capital gains tax when the investment is sold.

TFSA = Tax Free Savings Account

Graph and calculations courtesy of the Actuarial Society of South Africa

“If your children then leave their tax free savings accounts to grow until they turn 65, they would have the ultimate benefit of financial security well into retirement,” says Dempsey.

He adds that if these very fortunate children leave the R1.7 million invested they could retire with R6.1 million (adjusted for a 6% level inflation) at age 65, assuming the investment continued to earn net annual returns of 13%.

A taxable investment of R1.62 million on the other hand would grow to R5.3 million – R800 000 less than a tax-free savings investment.

“Anyway you look at it, gifting a tax free savings account has overwhelming benefit for your children over the long-term,” says Dempsey.

He points out that you do not need to invest the maximum of R2 500 a month to provide your children with this incredible gift. Some companies may require as little as R250 a month and even small amounts will make a difference.

Teenagers

Dempsey notes that unit trust investments could be particularly beneficial for teenagers as they move closer to the financial responsibilities of adulthood.

“Unit trusts are ideally long-term investments for terms of five years or longer,” says Dempsey. “And as your teens are a few years away from buying cars and houses, or starting to save for retirement, this is the perfect time to teach them about financial discipline and help them save for the future.”

The minimum amount you can invest varies between individual portfolios and is published in the fund fact sheets available from company websites. Some require minimum monthly investments as low as R50 or lump-sum investments of R500, while others require R500 monthly or lump-sum investments of R20 000.

“Investing in unit trusts is easy in practice, but because there are such a range of different types and portfolios available, consulting a trusted financial adviser is non-negotiable in order to make the best choice,” says Dempsey.

He explains that parents can invest in their child’s name, while taking responsibility for signing any necessary paperwork and making payments until their child comes of age.

Teens can then become involved in watching their investment grow, which he says will demonstrate to your children the benefits of practicing healthy financial habits and saving.

Partners

For partners that are not formally employed, Dempsey suggests that you could donate money to a retirement annuity (RA) in your spouse’s name.

Dempsey notes that RA investment returns do not attract tax, and are exempt from estate duties as well as protected by law against creditors, making them attractive investment vehicles.

He explains that while you would forfeit the tax incentive by not paying the money into your own annuity, you would be guaranteeing your spouse his or her own income into retirement.

“The future is uncertain, and by making an annuity investment in your spouse’s name, you are really offering them financial independence,” says Dempsey.

“Should you become insolvent or your relationship end, your partner will still have financial security in later years. An annuity may not sparkle, but it does demonstrate more meaningful thought and care for a loved one’s future.”

Dempsey notes that your financial adviser can guide you to the correct product for you and your partner’s needs.

Domestic workers

If you would like to provide a loyal domestic worker responsible for raising children with a meaningful gift, you could look into a Fundisa Fund, says Dempsey.

The Fundisa education unit trust fund aims to encourage South Africans to save for the higher education of children from lower-income families. Fundisa applies a means test of an annual household income of R180 000 or less to the families of the beneficiaries. The means test only applies to the families of the beneficiaries and not to the investors to ensure that high-income earners can invest on behalf of children from lower-income families.

Dempsey explains that the benefits of beneficiaries are enhanced by 25% every year to a maximum of R600 per learner. So if you save R200 each month for a beneficiary from a lower-income household for 12 months in the Fundisa Fund, you will see the R2 400 investment grow by R600 to R3 000. Furthermore, the R3 000 will also share in the overall investment return achieved by the fund in the next year.

“To gain maximum benefit from Fundisa, you would need to invest as little as R200 a month or R2 400 for the year,” says Dempsey. “But given the cost of education, any help you can offer could be hugely profound for the child as well as the family.”

For more information, see the Fundisa website at www.fundisa.org.za.

Secure your loved ones’ futures

According to the National Credit Regulator (NCR), South Africa’s consumer debt had risen to R1.63 trillion in June 2015, and of the 23.37 million credit active consumers, a staggering 10.5 million had impaired credit records.

“These statistics demonstrate South Africa’s culture of consumption,” says Dempsey. “Too many of us focus on instant gratification instead of the road ahead. The festive season is therefore the perfect time to show your family the rewards of saving and investing, and make a true difference to their lives.”

“Santa only comes one day a year, but you now have the power to give a gift that may shape your family’s entire financial future.”