ASISA: Life insurers paid 99.3% of underwritten life policy death claims worth R14.4 billion last year

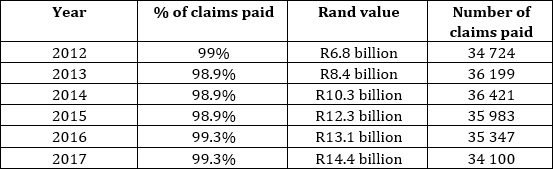

Life insurers paid 99.3% of all claims against fully underwritten life policies last year, resulting in benefit payments of R14.4 billion to beneficiaries following the death of a loved one.

Fully underwritten life policies are only issued if the policyholder has completed a full underwriting process, which involves a comprehensive assessment of the life insured’s health and medical history.

The 2017 annual death claim benefit statistics for fully underwritten policies released this week by the Association for Savings and Investment South Africa (ASISA) reveal that life insurers paid 34 100 death benefit claims, while only 238 claims to a value of R318.8 million were declined.

Hennie de Villiers, deputy chair of the ASISA Life and Risk Board Committee, says ASISA has been consolidating death benefit claims statistics for fully underwritten life policies since 2012 in order to provide consumers with the peace of mind that the majority of claims are paid.

“Since life companies exist primarily to provide consumers with the option of insuring themselves and their loved ones against the financial impact of an event like death, disability or disease, policyholders and their beneficiaries should be able to trust that their policies will pay when a life-changing event occurs.”

De Villiers says the death benefit claims statistics gathered over the past six years show that life insurers have a solid track record of paying benefits and delivering on their long-term promises to policyholders. He adds that the value of benefit payments over this period has more than doubled, despite a small drop in the number of claims submitted.

De Villiers adds that South African life insurers remain well positioned to deliver on long-term promises to policyholders. The long-term insurance industry continues to be well capitalised with assets exceeding liabilities by more than four times the legal reserve buffer.

Why claims were declined

Death claims against fully underwritten life policies will always be paid by insurers, provided the claim is not fraudulent and the policyholder did not:

• Commit suicide within the first two years of taking out the policy;

• Withhold important information from the insurer when applying for the policy; or

• Die as a result of an excluded condition.

De Villiers states that the primary reason supplied by life insurers for rejecting claims is non-disclosure, which involves an act of dishonesty on the part of policyholders.

• Non-disclosure

Non-disclosure refers to the failure of policyholders to disclose material information about a medical or lifestyle condition in an attempt to secure lower premiums or to obtain cover without exclusions.

Non-disclosure accounted for 50.4% of death benefit claims declined last year (55.3% in 2016).

De Villiers says it is encouraging that there has been a consistent decline in incidents of non-disclosure since 2012 when they accounted for 70.34% of claims rejected.

“Unfortunately, however, too many policyholders continue to take the risk of withholding information when applying for life cover at the expense of their beneficiaries.”

De Villiers explains that attempting to hide any medical conditions when applying for your life cover will place the value of your policy and the continued financial wellbeing of your family after your death at far greater risk than any potential exclusions you may face.

• Underwriting exclusions

De Villiers notes that by contrast to the number of claims declined for non-disclosure, only 12.6% of claims declined last year were as a result of the policyholder dying from a condition that had been specifically excluded by their life insurance policy (9.2% in 2016).

“This translates to less than 0.1% of all claims submitted, signalling that the overwhelming majority of policyholders died as a result of factors unrelated to an excluded health condition on their life policy last year. This highlights the importance of being upfront with your life insurer rather than jeopardising your policy pay-out,” he says.

A life company can apply an underwriting exclusion when, for example, the policyholder suffers from a specific illness such as diabetes, but is healthy otherwise. The life insurer may then exclude this condition from the life cover.

This means that if the policyholder is killed in an accident or dies of a cause unrelated to diabetes, for example, the life policy will pay. If the death is related to the excluded condition, the death benefit will not pay. Exclusions such as these allow insurers to provide life cover to people at affordable rates.

• Suicide

Incidents of claims declined due to suicide increased to 65 claims (27.3%) last year from 62 claims (23.7%) in 2016.

Life insurers generally apply a two-year exclusion period to suicide in order to prevent someone from taking out life cover with the intention of committing suicide shortly afterwards.

This means that if a policyholder commits suicide within the first two years of taking out life cover, no death benefit will be payable to the beneficiaries.

• Fraud

Claims declined due to criminal intent by either the policyholder or the beneficiary increased slightly to 7.6% of claims in 2017 (7.3% of claims in 2016).

Claims fraud usually involves the submission of fraudulent documentation and/or syndicate activity aimed at getting the life company to pay a claim to someone not entitled to the benefit.