Underwriting performance and strong investment results support Swiss Re half-year 2017 net income of USD 1.2 billion

• Group net income of USD 1.2 billion for the first six months of 2017; supported by disciplined underwriting and strong investment results • Property & Casualty Reinsurance net income USD 546 million; impacted by large natural catastrophe insurance claims • Life & Health Reinsurance net income USD 432 million; continued to report strong results • Corporate Solutions net income USD 39 million; started joint venture with Bradesco Seguros S.A. in Brazil • Life Capital gross cash generation at USD 532 million; open book activities continued to deliver attractive growth • High quality asset portfolio provided strong return on investments of 3.5% • Swiss Re's disciplined underwriting approach led to a stable year-to-date risk adjusted price adequacy for the renewed P&C Re portfolio at 102%

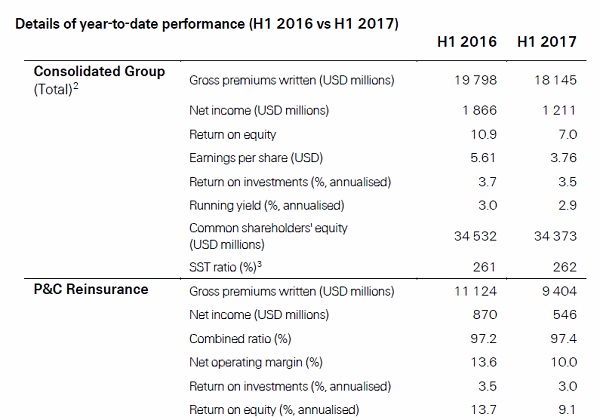

Swiss Re reported net income of USD 1.2 billion for the first six months of 2017. The result was supported by disciplined underwriting and strong investment returns, demonstrating that Swiss Re coped well with a business and market environment that continued to be challenging. The overall result was impacted by USD 360 million (net of retrocession and before tax) insurance claims in the aftermath of Cyclone Debbie in Australia. Based on the company's very strong capital position, Swiss Re is well positioned to respond to market opportunities while continuing to focus on its capital management priorities.

Swiss Re's Group Chief Executive Officer, Christian Mumenthaler, says: "In the first half of 2017, we reported a solid result – despite the challenging market environment and having paid significant claims in the aftermath of natural catastrophes. While in the short term these drivers, especially the pricing pressures, are concerning and are being addressed, we are steering our company with long-term value creation in mind."

Solid half-year results despite challenging market conditions Swiss Re reported net income of USD 1.2 billion for the first six months of 2017 supported by solid underwriting performance and strong investment results. The decline compared to the prior year was primarily driven by the absence of large one-off realised gains within the investment portfolio in Life Capital in 2016, which did not recur, as expected, in 2017.

The Group generated an annualised return on equity (ROE) of 7.0% in the first six months of 2017, with earnings per share (EPS) of CHF 3.75 or USD 3.76, compared with CHF 5.51 or USD 5.61 for the prior-year period. The Group's annualised return on investments (ROI) was 3.5% as the investment portfolio continued to provide strong and sustainable returns. The ROI was driven by net investment income as well as net realised gains, largely from sales of equity securities. The fixed income running yield was 2.9% consistent with the full-year 2016 running yield.

Gross premiums written for the half-year decreased 8.3% to USD 18.1 billion due to disciplined underwriting and active portfolio management.

Common shareholders' equity remained broadly stable at USD 34.4 billion as of 30 June 2017. Book value per common share was CHF 102.57 or USD 107.10 at the end of June 2017, compared with CHF 107.64 or USD 105.93 at the end of December 2016.

Swiss Re's capitalisation remains very strong, as shown by its Group SST 2017 ratio of 262%. Swiss Re believes it is well positioned to weather any headwinds while continuing to focus on its capital management priorities and to respond to market opportunities.

Swiss Re's Group Chief Financial Officer, David Cole, says: "While our property and casualty segments continued to experience pricing pressure in line with the overall industry and market environment, our life and health segments have delivered stable or even improved results. This shows the importance of having a diversified business model which can help to balance out volatility in individual areas. In addition, it is a differentiating factor that, together with our strong client relationships, can support our long-term value creation."

Solid P&C Reinsurance results despite challenging business environment

Net income in the first six months of 2017 was USD 546 million supported by a solid underwriting performance. Last year's net income benefited from positive foreign exchange movements which did not repeat in 2017. The result includes insurance claims from Cyclone Debbie in Australia of USD 320 million (net of retrocession and before tax).

The annualised ROE for the first half was 9.1% and the combined ratio remained stable at 97.4%, benefiting from favourable prior-year development.

Gross premiums written declined by 15.5% to USD 9.4 billion for the first six months of 2017. This was the result of a disciplined reduction in capacity where prices did not meet Swiss Re's profitability expectations.

July P&C Reinsurance treaty renewals show disciplined underwriting strategy

Following the July P&C Re treaty renewals, which focus mainly on the Americas, Swiss Re maintained an attractive portfolio. The treaty premium volume for the July renewals decreased by 10% and the year-to-date volume declined by 13%, as Swiss Re continued to allocate capital only to those opportunities that meet the Group's profitability criteria. The year-to-date risk adjusted price quality of the renewed portfolio was stable at 102%. The rate decreases for property and casualty reinsurance continued to slow down. Casualty rates remained generally more stable but with significant differences by market and product.

L&H Reinsurance delivered stable underwriting performance; strong 12.7% ROE

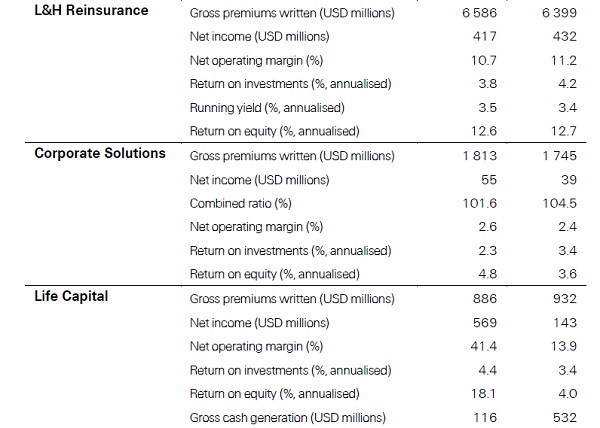

A stable underwriting performance generated USD 432 million in net income for the first six months of 2017. In addition, the result also benefited from higher realised gains and the annualised ROE was strong at 12.7%.

Gross premiums written declined 2.8% to USD 6.4 billion mainly due to changes in intra-group retrocession agreements and foreign exchange rate movements. New business growth continued with successful renewals and wins in the Americas and in Asia.

High growth markets are expected to see strong increases in primary life and health volumes and cession rates are expected to be stable. In Asia for example, Swiss Re expects the region's primary life insurance premiums to grow by 6%, in real terms per annum in the coming decade. L&H Re will continue to pursue business in high growth markets and in large transactions, including longevity deals. The rapid ageing of the world's population presents an opportunity to explore new ways to create affordable, accessible solutions and help ensure longer lives can be funded.

Corporate Solutions results impacted by high natural catastrophe losses and continued pricing pressure

The Business Unit generated a net income of USD 39 million in the first six months of 2017. The result was impacted by higher natural catastrophe losses compared to the same period of 2016 and continued pricing pressure, offset by income from investment activities. The combined ratio was 104.5% in the first six months of 2017, driven by high natural catastrophe losses, negative prior-year development and continued pricing pressure. The annualised ROE was 3.6%.

Gross premiums written1 decreased by 4.7% to USD 1.7 billion, impacted by cycle-related pricing pressure in most business segments.

In July 2017, Corporate Solutions commenced its announced joint venture with Bradesco Seguros S.A. in Brazil, creating one of the country's leading large-risk insurers, enabling innovative products to be delivered through an established distribution network.

The Business Unit continued to invest in its primary lead capabilities and further broadened its footprint by opening offices in Kuala Lumpur, Malaysia and Manchester, United Kingdom.

Life Capital delivered strong gross cash generation and made significant dividend payment to the Group

During the first six months of 2017, net income declined to USD 143 million. This decline was primarily driven by the absence of large one-off realised gains within the investment portfolio in 2016, which did not repeat, as expected, in 2017. The annualised ROE was 4.0%.

The Business Unit generated strong gross cash of USD 532 million during the first six months of 2017, driven by the underlying surplus on the ReAssure business and a benefit from the finalisation of the year-end statutory valuation. The strong capital position enabled Life Capital to make a significant dividend payment of USD 1.1 billion in the second quarter to the Swiss Re Group.

Gross premiums written increased by 5.2% to USD 932 million during the first half of 2017, due to growth in both the group and individual open life and health insurance business.

Life Capital will continue to pursue selective acquisition opportunities within the closed book market in UK while also growing its individual and group life and health business in Europe and the US. It aims to continue to generate significant cash while investing in its open book strategy.

Further integration of clear sustainability criteria into Swiss Re's investment strategy

In July, Swiss Re announced the implementation of benchmarks that systematically integrate environmental, social and governance (ESG) criteria into its investment decisions, as one of the first movers in the industry. This represents a step forward from considering ESG as an "add-on" approach to making it an integral part of Swiss Re's investment process. Swiss Re is convinced taking ESG criteria into account makes economic sense and reduces downside risks especially for long-term investors. Additionally, Swiss Re avoids investments in companies that generate 30% or more of their revenues from thermal coal mining or use at least 30% thermal coal for power generation. It has divested from all related equity positions and the vast majority of its fixed income holdings that meet this criteria.

Innovation continues to be at the core of Swiss Re

Technological advances will impact insurance risks and how insurance products will be distributed. Therefore, it remains a key priority for Swiss Re to stay ahead of industry developments. In July, Corporate Solutions launched Insur8, the first-ever typhoon warning insurance product for businesses operating in Hong Kong. This new product indemnifies local businesses against loss of earnings caused by forced shut-downs and additional operating costs stemming from a signal 8 or above typhoon warning issued by the Hong Kong Observatory.

The first half of the year also saw the launch of World Bank bonds that will support the Pandemic Emergency Financing Facility (PEF) – a pioneering instrument to channel first-response surge funding to developing countries facing the risk of a pandemic. Swiss Re Capital Markets Ltd. is a joint structurer and the sole book-runner for the cat bond transaction. This marked the first time pandemic risk was being transferred to the capital markets to cover low-income countries.

Group Chief Executive Officer Christian Mumenthaler says: "We acknowledge that the market environment remains difficult. At the same time, we take decisive measures addressing the industry challenges head on. We will continue to be selective in choosing the risks we underwrite, aiming to ensure future profitability. We are equally determined to put our knowledge and leadership position to work and collaborate with our clients. I am confident the long-term trends for our industry are positive as risk pools will continue to grow."