Swiss Re sigma study

Swiss Re sigma study on world insurance in 2012 shows premium growth resumed, reaching 2.4% despite a very challenging economic environment.

• Non-life premium growth picked up to 2.6% in 2012, while life premiums resumed growth, rising by 2.3%. Overall premium volume expanded, but developments in Western Europe, China and India weighed on the result.

• Premium growth will likely improve further in the near term. The gradual hardening of prices in non-life insurance is likely to broaden and deepen. In life insurance, China and India are expected to rebound in 2013. However, the weak economy in the Eurozone will remain a drag on insurance demand in the region.

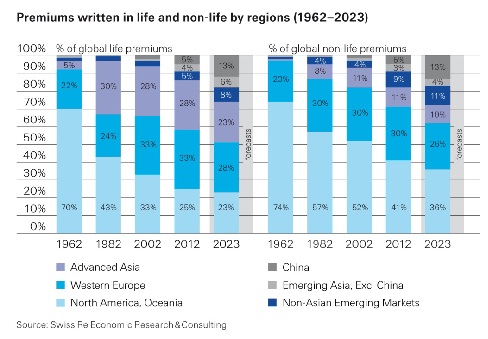

• Asian insurance markets will continue to rise in importance over the next 10 years. In the very long-run, projected population patterns suggest that Africa could become the next star of the industry.

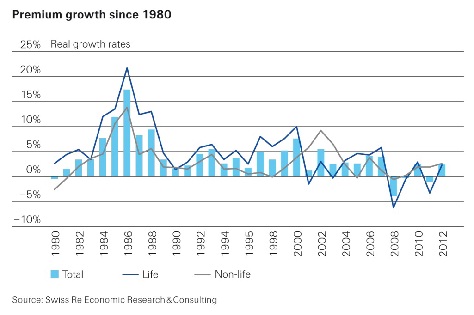

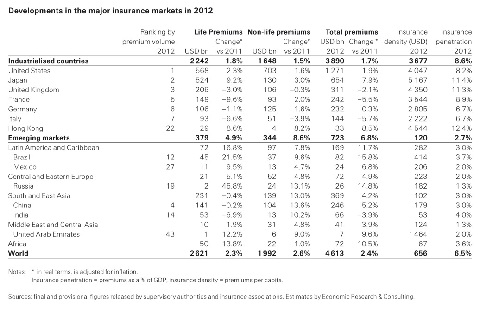

Swiss Re’s latest sigma study reveals that total global premiums written increased by 2.4%0F1 in real terms in 2012 to USD 4 613 billion. Life premiums expanded by 2.3% unwinding some of the contraction in 2011, thanks to improvements in emerging markets and solid demand in the US and advanced Asian markets. In non-life, premiums rose by 2.6% on the back of continued economic expansion in emerging markets and selective price increases in some advanced markets. Profitability of life insurers remains subdued but non-life underwriting results improved modestly. Low interest rates continue to depress investment income, but are boosting reported accounting capital and solvency levels under GAAP.

Life premiums increased by 2.3% worldwide

Global life insurance premiums increased by 2.3% in 2012 to USD 2 621 billion after contracting by 3.3% the previous year. While the increase is encouraging, growth remains below the average pre-crisis rate. Life premium volume increased 4.9% in emerging markets. This came after a sharp decline in 2011 due to contractions in India and China following changes to regulations relating to insurance distribution. In advanced markets, growth was 1.8% (2011: 3%), largely supported by robust performance in advanced Asian markets and the US, while life insurance markets in Western Europe continued to shrink.

Non-life premium growth picked up in 2012

Premium volume for non-life business increased by 2.6% in 2012 to USD 1 992 billion (2011: 1.9%). However, this is still less than the average pre-crisis growth rate. In emerging markets, non-life premiums expanded by 8.6% in 2012 (2011: 8.1%). The recovery in the advanced markets gained momentum with growth picking up to 1.5% (2011: 0.9%), the fourth consecutive year of rising premiums following the decline in 2008.

Daniel Staib, one of the authors of the study, says: "Premium growth held up well given the challenging economic environment. The non-life market was supported by steady increases in risk exposures in emerging markets and by selective premium rate increases in some advanced markets, particularly in Asia."

Staib continues: "In terms of profitability, the historically low level of interest rates continues to be a problem – particularly for life insurance companies. Alongside increases in revenues, profitability in non-life improved moderately backed by benign catastrophe losses and reserve releases. At the same time, the industry remains well capitalized, even though GAAP figures overstate current capital levels because of low interest rates."

Outlook: Premiums will continue to increase but at a moderate pace

"Premium growth expectations for the short-term remain below pre-crisis trends. In life, the expansion in emerging markets will likely accelerate as insurers in China and India adapt to the new regulatory environment, but the weakness in Western Europe will dampen developments in advanced markets. The non-life side is more positive since the sector will benefit from the strong economic performance of emerging markets and selective rate increases in advanced markets. However, rate increases will likely be moderate given the prevailing surplus capacity in the markets," says Mahesh Puttaiah, one of the authors of the study.

Long-term trends: shift to Asia to continue - next star Africa?

Economic growth and rising penetration will continue to increase the emerging market share of total premiums over the next ten years. Ageing populations will boost demand for life insurance products also in emerging markets, while non-life insurance will profit from increasing urbanisation, an expanding middle class and rising economic wealth.

Kurt Karl, Swiss Re’s Chief Economist, points out: "The rise in importance of emerging Asia in the global economy and insurance markets witnessed over the past 20 years is set to continue for at least another decade. However, demographic patterns suggest that by 2062, Asia's share in the world population will actually decrease from 60% to 53%, mainly due to the developments in China, where the working age population will start to contract from 2018. At the same time, Africa's population share is projected to increase from 15% currently to roughly 27%.

This positions Africa well, from a demographic point of view, to become an important part of the global insurance markets over the next fifty years."

This sigma study is the first comprehensive assessment of the performance of global insurance markets in 2012. The 79 markets where data or estimates for 2012 are available, account for 99.2% of global premium volume. Overall, the report is based on 147 insurance markets.