Swiss Re's insurance outlook for 2014/15 sees emerging markets driving premium growth, while alternative capital focuses on well-modelled risks

29 November 2013 | Company News & Results | Swiss Re | Swiss Re

? Global economic strengthening will continue in 2014 ? Real primary market non-life premium growth is projected to be 2% in the advanced and 8% in emerging markets in 2014 ? Robust emerging market growth will boost global primary life premiums by 4% in 2014 and 2015 in real terms ? Life reinsurance premiums in advanced markets are expected to shrink in 2014 ? Alternative capital will remain focused on transparent, well-modelled Nat Cat business

Global economic growth will continue to strengthen in 2014, Swiss Re says in its "Global insurance review 2013 and outlook 2014/15". This will support on-going premium growth in the non-life primary market, particularly in emerging markets, with reinsurance premiums following suit. Global premiums in the life market are expected to grow by around 4% in real terms in 2014 and 2015. However, life reinsurance premiums are expected to continue to decline in advanced markets, while rising by about 6% annually in emerging markets. Alternative capital has increased in recent years, putting pressure on prices and margins, particularly in the US catastrophe business. The alternative funds are expected to maintain a focus on established nat cat markets.

The momentum in global economic growth achieved this year will continue into 2014. The US economy is still growing and the euro area, while not expected to accelerate rapidly, has returned to growth. The weaker yen has boosted growth and increased inflation in Japan, but the sustainability of this recent economic strength is uncertain. China's growth trend is close to 7.5%, down from 10% previously.

Emerging markets to drive non-life insurance sector growth

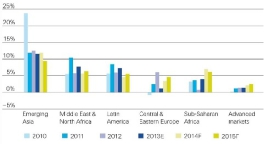

The gradual improvement in economic activity in key markets has supported continued growth in non-life premium rates. Real (after-inflation) premium growth in the primary market is projected to be around 2% in the advanced economies, and close to 8% in the emerging markets in 2014. Premium growth in the reinsurance sector will follow suit, but be a little stronger. The low interest rate environment has weighed on investment returns in the primary life market. Reinsurers have been similarly impacted, with sector profitability estimated to be close to 10% in 2013, down from 14% in 2012.

Kurt Karl, Swiss Re's Chief Economist says: "A return to economic growth in the mature markets is a good sign for insurance and we see a positive outlook for the next two years. Emerging markets, especially in Africa and Asia, will definitely provide some of the more spectacular growth figures in non-life business as cities grow and people look for financial protection for their property."

The recent Typhoon Haiyan disaster in the Philippines is unlikely to generate large losses for non-life insurers. This is because of the very low insurance penetration in the Philippines, currently at around 0.5% compared with an emerging market average of about 1.3%.

Figure 1: Real premium growth rate for primary non-life insurance by region, 2010 to 2015F

Global life sector recovery to continue, but reinsurance premiums in advanced markets expected to shrink

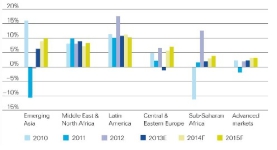

Global primary life premiums have continued to recover this year, with emerging market real premium growth above 6% and advanced market growth at 2.3%. Global life premium growth is projected to rise to around 4% in 2014 and 2015, fuelled by robust emerging market growth on the basis of rising incomes and increased insurance awareness.

Life insurance premium growth has rebounded sharply in emerging Asia, growing by about 6% in real terms this year.

Karl says: "The figures for emerging markets this year have been robust and this is expected to continue. In Latin America, we saw 18% growth in 2012 and in 2013 we are looking at 10% growth, which is still very good."

Economic activity in the stable countries of the Middle East and North Africa region is supporting above-5% growth in life premiums, but from a very low base.

Figure 2: Real premium growth rate for primary life insurance by region, 2010 to 2015

In the life reinsurance sector, premiums in the emerging markets are expected to grow by 6% annually over the next few years. In these markets, reinsurers’ main value proposition will be to support their primary insurance clients in product development, underwriting and claims management. However, in the advanced markets, life reinsurance premiums are expected to continue to decline as regulatory changes reduce demand in the US and to a lesser degree in the UK. Other advanced markets are expected to fare better.

Alternative capital will focus on well-modelled risks

Alternative capital, which is Natural Catastrophe (Nat Cat) capacity provided by Insurance Linked Security (ILS) Funds, Mutual Funds, Pension Funds, Hedge Funds and Private Equity, has increased sharply in recent years. These alternative capital providers focus mostly on the US reinsurance business and retrocession, and the inflow of capital has put margin pressure on US Cat business. However, the staying power of these new investors has yet to be tested by a rise in interest rates, decreasing ILS returns or large catastrophe losses.

It is expected that alternative capital providers will continue to focus mostly on the US reinsurance business, where well-modelled risks, low entry barriers and relatively high margins characterise the market.

"Investors need well-modelled and transparent risks to invest in," says Martin Bisping, Head of Non-Life Risk Transfer at Swiss Re. "We can expect funds to focus on established nat cat markets where the conditions are well understood – at the moment this means the US is the most attractive market."