Swiss Re reports full-year 2017 net income of USD 331 million despite USD 4.7 billion of natural catastrophe losses

• Group net income of USD 331 million despite the large natural catastrophes, making 2017 one of the costliest years for the re/insurance sector in history • Combined estimated claims from large natural catastrophes for Swiss Re amounted to USD 4.7 billion in 2017 • Property & Casualty Reinsurance net loss USD 413 million; estimated natural catastrophe insurance claims of USD 3.7 billion • Strong Life & Health Reinsurance net income USD 1.1 billion; ROE of 15.3% • Corporate Solutions net loss USD 741 million; estimated natural catastrophe insurance claims of USD 1.0 billion • Life Capital net income USD 161 million; strong gross cash generation of USD 998 million • Very strong investment performance; ROI 3.9% and 2.9% running yield • January 2018 renewals premium volume up 8%; prices increased by 2% • Board of Directors to propose a higher dividend of CHF 5.00 per share; share buy-back 2017 completed; Swiss Re to seek authorisation for a new public share buy-back programme

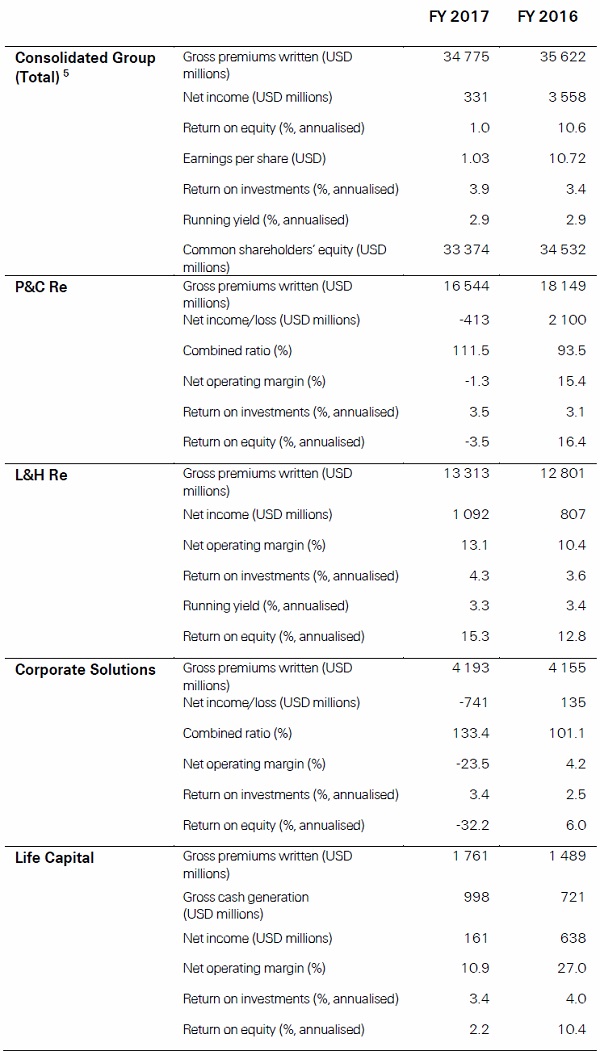

Swiss Re’s full-year net income declined to USD 331 million in 2017. The result includes estimated insurance claims, net of retrocession and before tax, of USD 4.7 billion from large natural catastrophes, such as Cyclone Debbie in Australia, Atlantic hurricanes Harvey, Irma and Maria, the Mexican earthquakes, and the wildfires in California. Both Property & Casualty Reinsurance (P&C Re) and Corporate Solutions results were significantly affected by these events. P&C Re posted a full-year net loss of USD 413 million in 2017, and Corporate Solutions incurred a net loss of USD 741 million. Life & Health Reinsurance (L&H Re) increased its net income to USD 1.1 billion, driven by solid underwriting results and strong investment performance. Life Capital generated gross cash of USD 998 million. Swiss Re’s investment performance for 2017 was very strong, with a return on investment (ROI) of 3.9%. Despite the high losses in 2017, Swiss Re Group’s economic solvency remains very strong and comfortably above the Group’s respectability level of 220%.

Swiss Re Group Chief Executive Officer, Christian Mumenthaler, says: “The severe natural disasters of 2017 are not only loss events, they are above all human tragedies and we are deeply moved by the devastation caused. In times like these we demonstrate the critical role re/insurance plays in enabling people and economies to recover. I am proud that Swiss Re, also through our clients, will be supporting people and businesses affected with estimated payouts of USD 4.7 billion. 2017 proved how our strategy to maintain a superior capital position and pursue disciplined underwriting continues to be the right approach.”

2017 dominated by natural catastrophes

After Cyclone Debbie in March, hurricanes Harvey, Irma, and Maria and the Mexican earthquakes caused considerable damage during the third quarter of 2017. During the last quarter of the year, wildfires in California resulted in additional estimated insurance claims for Swiss Re of USD 0.4 billion. As a result of the estimated combined claims of USD 4.7 billion from natural catastrophes, Swiss Re’s net income declined to USD 331 million. The result reflects a USD 93 million benefit from the US tax reforms.

The Group ROE for 2017 was 1.0%. Earnings per share (EPS) were USD 1.03 or CHF 1.02, compared to USD 10.72 or CHF 10.55 in the previous year. Gross premiums written for the Group decreased by 2.4% to USD 34.8 billion. In P&C Re, gross premiums written declined due to active portfolio management and continued underwriting discipline. In L&H Re, gross premiums written increased driven by new business wins in Asia and the Americas, including a number of large transactions.

Swiss Re’s investment portfolio continued to demonstrate its successful sustainable investment strategy with another very strong contribution. All asset classes helped to achieve the result, reflecting the diversification of income sources as well as the quality of the investment portfolio. The Group’s annualised ROI was 3.9%. The higher return compared to the previous year was supported by additional realised gains from the sale of equity securities (including select divestments in Principal Investments). In 2017, Swiss Re increased its overall allocation to government bonds and credit investments, alongside a reduction of cash and short-term investments, enhancing income with low duration risk. In turn, net investment income slightly increased compared to the prior year.

Common shareholders’ equity changed compared to the previous year by –3.4% to USD 33.4 billion at the end of 2017. The decline mainly reflected a payment to shareholders of USD 2.6 billion for the 2016 regular dividend and the share buy-back programmes. Book value per common share was at USD 106.09 or CHF 103.37 at the end of 2017, compared to USD 105.93 or CHF 107.64 at the end of 2016.

Swiss Re Group Chief Financial Officer, David Cole, says: “The 2017 results clearly show the strength of our diversified business model. The losses in our P&C businesses were offset by strong results in our life and health businesses, further supported by our investment performance. Our capital position remains very strong and we continue to have ample financial flexibility to invest in future growth and business opportunities as they arise.”

Increased dividend of CHF 5.00 per share and new share buy-back programme proposed

Swiss Re’s Board of Directors will propose a higher dividend of CHF 5.00 per share for 2017. The dividend will be paid after shareholder approval at the Annual General Meeting (AGM) on 20 April 2018.

Consistent with its objective of returning capital to shareholders when excess capital is available and other business opportunities do not meet profitability requirements, Swiss Re launched its previously authorised public share buy-back programme of up to CHF 1.0 billion purchase value on 3 November 2017. It was concluded on 16 February 2018.

In line with the above-mentioned capital management priorities, Swiss Re plans to continue to return excess capital to shareholders. The Board of Directors will propose to the AGM a further public share buy-back programme of up to CHF 1.0 billion, commencing at the discretion of the Board of Directors after the AGM’s approval and subject to the necessary regulatory approvals having been obtained. Unlike prior years, beyond the Board and regulatory approval and considering the capital management priorities, there will be no other preconditions to the commencement of the proposed share buy-back programme.

P&C Re results affected by high natural catastrophe losses; focus on innovative solutions for its clients

Estimated combined claims of USD 3.7 billion from 2017’s large natural catastrophes led to a strong decline in P&C Re’s results. The net loss for 2017 amounted to USD 413 million and the annualised ROE was –3.5%.

The combined ratio increased to 111.5%, reflecting the impact from the significant natural catastrophes. P&C Re continued to experience positive prior-year development in 2017.

Amid a continued challenging market, Swiss Re maintained its strict disciplined underwriting approach, ensuring it receives adequate prices for the protection it provides. This active reduction in capacity resulted in an 8.8% decline in gross premiums written to USD 16.5 billion in 2017.

During the year, P&C Re continued to strengthen its differentiation as a full-service solutions provider and long-term partner for its clients. In this, technology plays an important part. One example of such technology-based solutions is a machine-learning-based pricing platform that Swiss Re has developed to accurately price risks, make the online purchase of insurance policies simple and easy and enable automated payments of claims. This platform can be leveraged for multiple parametric insurance products, such as those covering earthquakes or delayed airline flights.

Another example of such client-oriented solutions is the launch of “OptiCrop”, a fully white-labelled web-based application. It allows farmers to assess current and past conditions of their crops, compare their fields to their neighbours’, track index policies and receive precipitation forecasts. In the future, it will allow farmers to monitor soil moisture and directly request parametric insurance policies for their fields. The solution is already being used in parts of China, Africa, Ukraine and Latin America.

L&H Re delivered another year of strong performance

L&H Re delivered a strong net income of USD 1.1 billion in 2017, driven by a stable underwriting result and strong investment performance, which generated an annualised ROE of 15.3%. The fixed income running yield for the year remained stable at 3.3%.

Gross premiums written for 2017 increased by 4.0% to USD 13.3 billion, mainly due to new business wins and growth in all markets, including a number of large transactions in the US and Asia.

Also in L&H Re, technology-enabled solutions played an important role in 2017. In line with the Business Unit’s strategy to continue to drive innovation, the L&H underwriting competencies in document analytics were strengthened. This enables automatic content identification and extraction to simplify the handling of non-digital and unstructured data input. It also aims at making claims interactions with clients more seamless.

Going far beyond the traditional capital offering for clients, L&H Re received a very positive response to its award-winning Cancer Work Support Service in the UK market, which provides rehabilitation support to people who are living with and recovering from cancer. The service is currently provided to more than 10 Swiss Re clients in the UK, reaching more than 400 individuals. Swiss Re is proud to have partnered with AIA Australia to introduce a similar service in Australia.

Corporate Solutions’ results significantly impacted by natural catastrophes; keeps financial flexibility to invest in future growth

Corporate Solutions reported a net loss of USD 741 million in 2017. The result was significantly impacted by the natural catastrophes in the United States – Corporate Solutions’ largest market – the Caribbean and Mexico. As a leader in excess layers1 and a large net capacity provider2, Corporate Solutions’ results are subject to higher volatility.

The ROE for 2017 was –32.2% while the combined ratio increased to 133.4%. Gross premiums written3 remained broadly unchanged at USD 4.1 billion.

With Corporate Solutions, Swiss Re has built a platform to access the large pool of commercial risks. During the fourth quarter, the Group strengthened Corporate Solutions’ capital position, underlining its commitment to the commercial insurance market and Swiss Re’s confidence in the unit’s long-term strategy. This equips Corporate Solutions with the necessary financial flexibility to write future profitable business, as the outlook for the commercial insurance market has improved following the recent natural catastrophes.

In 2017, Corporate Solutions continued to make progress on its long-term strategy, with investments into its Primary Lead capabilities4 and office openings in Kuala Lumpur and Manchester, UK. The start of the Bradesco joint venture in Brazil – now one of the leading large-risk insurers in the country – is timely as economic indicators in the country are improving.

Life Capital delivered strong gross cash generation; significant growth in its open book business

Life Capital delivered significant gross cash generation of USD 998 million, driven by strong underlying surplus and further benefitting from an update to mortality assumptions and the finalisation of the 2016 year-end Solvency II statutory valuation. The 2017 net income was USD 161 million, benefitting from realised gains on sales and favourable UK investment market performance. As expected, large one-off realised gains on the investment portfolio in the prior-year period were not repeated in 2017. The annualised ROE decreased to 2.2%.

Gross premiums written in 2017 increased by 18.3% to USD 1.8 billion, mainly driven by significant growth in the open book business.

In October 2017, Swiss Re reached an agreement with MS&AD Insurance Group Holdings Inc (MS&AD) for an investment of up to GBP 800 million in ReAssure (its closed book business) for up to a three-year period from closing and with a maximum shareholding of 15%. On 23 January 2018, after ReAssure obtained regulatory approval for the transaction, MS&AD acquired a 5% stake in ReAssure for GBP 175 million and subscribed for additional shares in the amount of GBP 330 million. These two investments now result in a total shareholding by MS&AD in ReAssure (via a parent company) of 13.2%.

In December 2017, Swiss Re agreed to purchase 1.1 million life insurance policies from UK financial service provider Legal & General Group PLC (L&G) for GBP 650 million. This is consistent with Swiss Re’s strategy to acquire closed life books in the UK and further strengthens its market position.

In the open book business, Life Capital continued to invest in technology and its platforms during 2017, to position both elipsLife and iptiQ for growth opportunities in their respective businesses.

Improved outlook for P&C Re following January 2018 treaty renewals

Swiss Re renewed USD 8.1 billion compared to the USD 7.5 billion premium volume up for renewal on 1 January 2018. This represents an increase of 8%, driven by higher rates across all major lines of business and regions and new large transactions. Prices increased by 2%. Improvements were most pronounced in the loss-affected property lines and were more moderate in other lines. Risk-adjusted price quality increased to 103%. The majority of the loss-affected US property business will be up for renewal later in the year.

Swiss Re in discussions with SoftBank

On 7 February 2018, Swiss Re confirmed that it is engaged in preliminary discussions with SoftBank Group Corp., which approached Swiss Re regarding a potential partnership and minority investment. Swiss Re's Board of Directors is carefully assessing the strategic and financial implications of such a partnership, having in mind the best interests of the company and its shareholders. Swiss Re's capital position remains very strong; the issuance of new capital is not under consideration. There is no certainty that any transaction will be agreed, nor as to the terms, timing, or form of any transaction.

Pushing boundaries in innovation

In March 2017, the Swiss Re Institute was launched – bringing together Swiss Re’s research and development capabilities under one roof. Through valuable R&D, the Institute helps identify new opportunities for both Swiss Re and its clients and represents an important differentiator. The launch of the Swiss Re Institute symbolises a further step on Swiss Re’s journey and strengthens its position as a risk knowledge company that invests in risk pools. This means Swiss Re applies its knowledge and works alongside its clients to develop innovative ways to extend insurance coverage to more people and businesses.

Group Chief Executive Officer, Christian Mumenthaler, says: “2017 was clearly a challenging year for the industry – and Swiss Re. However, we believe the outlook for our industry is now more positive than it has been during the last four years. Changes in the market environment, such as adjusting property and casualty price levels and increases in interest rates, are expected to be beneficial for our business. In addition, the catastrophes are a reminder of the relevance of large global re/insurers and their role in tackling the large worldwide insurance protection gap. It visibly shows that the need for insurance is increasing due to developments such as population growth and the concentration of assets in catastrophe-prone regions.”

Details of year-to-date performance (FY 2017 vs FY 2016)