Swiss Re posts another strong quarterly profit of USD 802 million, contributing to a half-year net income of USD 2.0 billion

• Strong re/insurance business and excellent asset management performance resulting in a quarterly profit of USD 802 million, slightly up in comparison to Q2 20131 • P&C Re H1 2014 net income of USD 1.5 billion driven by continued good underwriting • Successful July renewals with higher premium volumes and year-to-date risk adjusted price quality of 108% • L&H Re H1 2014 net income of USD 112 million, management action underway to achieve targeted profitability level • Corporate Solutions H1 2014 net income of USD 146 million, with growth from most business lines • Admin Re® excellent cash generation and H1 2014 net income of USD 165 million • Return on equity of 12.6% and earnings per share of USD 5.92 for H1 2014 show steady progress toward 2011–2015 financial targets

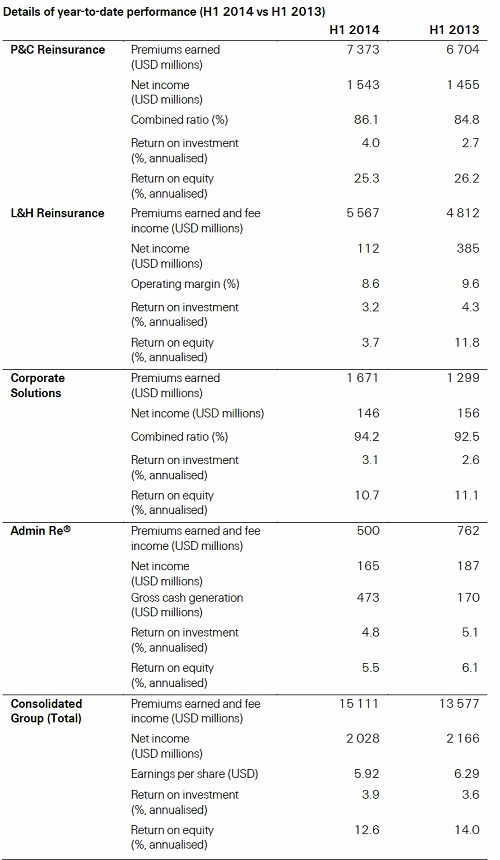

Swiss Re Group reports net income of USD 2.0 billion for the first half of 2014. All business segments contributed positively in the second quarter to this result, with strong underwriting performance by Property & Casualty Reinsurance, steady growth from Corporate Solutions and excellent gross cash generation by Admin Re®. Asset Management also demonstrated excellent year-to-date performance with an investment result of USD 2.2 billion.

Michel M. Liès, Group CEO, says: "USD 2.0 billion profit in the first six months of 2014 is an impressive result. I'm especially pleased as it demonstrates our strong client relationships, and obviously translates well into shareholder value. We see the insurance market generally softening. Thanks to our leading position we continue to take advantage of opportunities as they arise – for example in high growth markets – and actively manage our overall portfolio. I am confident that Swiss Re will remain successful at every stage of the cycle."

Group continues with successful strategy through first half of 2014

All Business Units have contributed in the second quarter to deliver a net income of USD 2.0 billion for the first half of 2014 (vs. USD 2.2 billion in H1 2013). The excellent year-to-date Group return on investments of 3.9% was largely the result of last year's successful asset re-balancing. The re-balancing led to higher investment returns and more diversified sources of income while still maintaining a high-quality asset portfolio.

The annualised return on equity for the six months now stands at 12.6%, with earnings per share of USD 5.92. The Group remains well on track to meet its 2011–2015 financial targets. Book value per common share rose to USD 95.06 or CHF 84.30 compared to USD 93.08 or CHF 82.76 as of 31 December 2013.

Strong second quarter performance across the Group

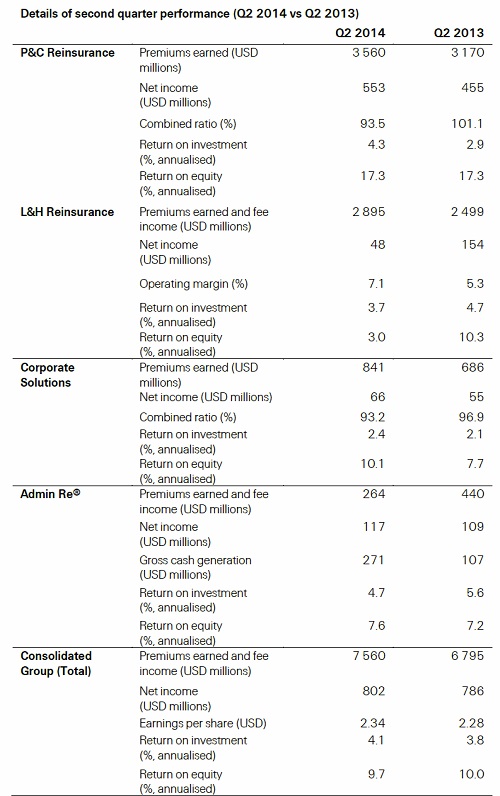

For the second quarter P&C Re delivered a net income of USD 553 million (vs USD 455 million in the second quarter of 2013) and premiums earned rose by 12.3% to USD 3.6 billion (vs USD 3.2 billion). Net income in L&H Re was USD 48 million, with premiums earned and fee income 15.8% higher at USD 2.9 billion.

Corporate Solutions second quarter net income was USD 66 million (USD 55 million); net premiums earned were 22.6% higher at USD 841 million. Admin Re® delivered a net income of USD 117 million for the quarter. The Group return on investment for the quarter was a very strong 4.1%.

David Cole, Group CFO says: "I'm pleased how 2014 has been shaping up so far. Our results show the fundamental strength of the Group's business model and strategy. All Business Units have delivered an improved performance against their key metrics in the second quarter. Also L&H Re improved its operating margin in comparison to the prior-year period, as promised; however, there is still lot of work to be done in this segment. Meanwhile, Admin Re® generated substantial cash for the Group – USD 271 million in the second quarter of 2014."

P&C Re leading with core strengths

P&C Re delivered net income of USD 1.5 billion over the first six months of the year. This performance is built on continued underwriting excellence through a relatively benign natural catastrophe period, leading to a half-year combined ratio of 86.1% (compared to 84.8%in H1 2013). Premiums earned rose by 10.0% to USD 7.4 billion (vs USD 6.7 billion), benefiting from the expiry of a major quota share agreement at the end of 2012 and large Asia and Americas transactions written at the end of 2013. Active management of the equity portfolio also drove these strong results.

L&H Re confirms 2015 RoE target

L&H Re net income for the six months was USD 112 million (vs USD 385 million in H1 2013). Premiums earned and fee income were 15.7% higher at USD 5.6 billion, with health business in Asia and EMEA contributing to continued growth. The operating margin was 8.6% (vs 9.6%).

L&H Re management is working across all lines of business to achieve the targeted profitability level.

Corporate Solutions again delivers profitable growth

Corporate Solutions generated net income in the first six months of USD 146 million (vs USD 156 million in H1 2013). Most lines of business saw growth in premium volume leading to net premiums earned of USD 1.7 billion, 28.6% higher than in the first half of 2013. The combined ratio increased from 92.5% in H1 2013 to 94.2% in H1 2014.

As announced at the Investors' Day on 3 July 2014, Corporate Solutions will focus on developing primary lead capabilities and its position in a number of high growth markets to continue its growth. Corporate Solutions has agreed to acquire the insurer Sun Alliance Insurance (China) Limited, representing another milestone in the high growth market ambitions. The acquisition, once completed, will enable Corporate Solutions to offer corporate insurance directly from mainland China.

Admin Re® generates substantial cash for the Group

Admin Re® delivered net income of USD 165 million in the first half of 2014 (vs USD 187 million in H1 2013) and gross cash generation of USD 473 million (USD 170 million). This underlines the Business Unit's position as a strong and secure cash earner for the Group. It also confirmed the commitment of Admin Re® to the UK market with the acquisition of pension and annuity policies from HSBC, as announced in June.

Successful July renewals in a challenging environment

The July treaty renewals, which focus on the Americas and the Australia and New Zealand region, were successful, especially casualty, which grew further on profitable terms. Swiss Re wrote less nat cat business, but did so at attractive price levels. The July treaty renewal premium volume grew by 8%. Year-to-date treaty renewals show a growth of 4% with year-to-date risk adjusted price quality at 108%.

Steady progress toward 2011—2015 financial targets

The Group is well on track toward achieving its 2011—2015 financial targets. The annualised return on equity for the six-month period is 12.6% and earnings per share are USD 5.92. The new set of targets covering 2016 and beyond will be announced in February 2015.

Michel M. Liès says: "It is an exciting but also demanding time for the re/insurance industry. The environment is heavily influenced and shaped by various megatrends, such as the continuous insurance demand in high growth markets, increasing regulation or big data. I believe big data has the potential to actually revolutionise not only our industry but the entire economy. Hence we keep a close eye on its development, consider business opportunities and establish dialogue platforms around big data at events such as "Les Rendez-vous de septembre", when the global property and casualty industry meets in Monte Carlo."