New Swiss Re sigma study looks at 21 frontier markets that will provide the next wave of insurance growth

• Sigma report identifies 21 markets in Sub Saharan Africa, Latin America, the Commonwealth of Independent States and Asia with the right mix of conditions for insurance growth • Common features include GDP growth rates of 5-10% and low insurance penetration rates of less than 1.5% • There is no "one-size-fits-all" approach; insurers need to navigate differing regulatory regimes, cultural characteristics and economic situations • Frontier markets require a long-term commitment; there is a significant first-mover advantage for insurers who understand the markets and can position themselves for growth

Behind the excitement created by the leading emerging markets such as Brazil, India or China, there is a group of "frontier markets" which have a promising outlook for economic growth and offer attractive long-term potential for insurers. Swiss Re's latest sigma study looks at 21 frontier markets such as Nigeria, Ecuador, Vietnam and Azerbaijan. It provides an outlook for premium growth and an overview of the economic fundamentals which will lead to increased demand for insurance in these countries. The report also looks at the individual features of each market, covering topics such as impending regulatory changes and the influence of external factors such as regional trade agreements.

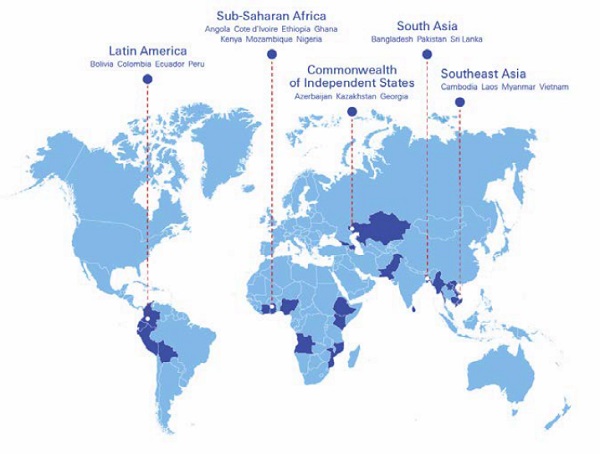

Frontier markets are typically those emerging countries with smaller-sized economies, lower income levels and insurance sectors in the early stages of development. Across these markets, annual real gross domestic product (GDP) growth is forecast to be strong (5% to 10%) in the near term, and total insurance penetration rates are less than 1.5%, pointing to significant catch-up potential. Most of the markets are in Sub-Saharan Africa (SSA). The sigma report also assesses frontier markets in the Commonwealth of Independent States (CIS), Latin America and Southeast Asia.

"Capturing the potential in frontier markets will require a long-term strategy. Nonetheless, this work shows that there is a real "early-mover" advantage to be gained for insurers who understand how to access and develop these markets," says Swiss Re Chief Economist Kurl Kart. "The benefits will come once these markets reach the critical middle-income threshold when consumers and businesses start buying more insurance."

Opportunities and challenges for insurers

Swiss Re's report identifies a typical growth pattern for insurance within frontier markets. In the initial years, growth will likely favour non-life and commercial business over life and personal lines. Later, as incomes rise, premiums for life products, with their emphasis on savings, could grow more rapidly. However, there is no "one-size-fits-all" approach to increasing insurance penetration or doing business in the frontier markets. To be successful, insurers will need to understand the different macroeconomic conditions, socio-economic factors, regulatory regimes and cultural characteristics of the various markets.

The report looks at how insurers can access the markets. For example, it analyses the advantages and disadvantages of joint ventures between international and local insurers. It also highlights the opportunities in markets which already have tech-savvy consumers, such as how to leverage digital distribution and the role of simple, easy-to-understand products. An important consideration is how the deployment of technologies can disrupt the established growth path for insurance and allow some markets to leap-frog to a higher stage of development.

An overview of the frontier markets: Sub Saharan Africa (SSA)

SSA is a diverse region consisting of 48 independent states. Despite overall solid growth since the turn of the century, GDP per capita remains low across SSA. Since 2000, real premium growth in the SSA frontier markets has been lower than real GDP growth, dampened by years of political instability and civil war, which affected the insurance sector more than economic growth.

Although the report focuses on seven of the top frontier economies in the region, all markets in Sub-Saharan Africa, with the exception of South Africa, can be considered frontier markets. Insurance penetration is generally low as the markets are mostly in the early stages of development and insurance for commercial risks (e.g., construction, mining, oil and gas) dominate. Motor insurance is gaining importance due to increasing enforcement of compulsory motor third-party liability (MTPL) cover in many countries.

Regulatory frameworks and supervision have been improving, but are often still weak. On the other hand, SSA is leading the emerging markets in terms of mobile-phone distributed (micro) insurance. With the large low income population, micro-insurance and mobile-based insurance products will be key to increasing the reach and penetration of insurance. Other growth areas are in the agriculture field and insurance for large infrastructure projects.

Commonwealth of Independent States (CIS)

In CIS countries, the insurance sector remains underdeveloped. To some extent, this reflects the prevailing mindset of relying on state or family support in the time of need: many people in the CIS countries see insurance as a luxury. However, insurance growth has also been impacted by volatile economic developments in recent years. Most notably, the collapse in commodity prices highlighted the lack of diversification in these economies.

Nevertheless, the long-term economic and insurance sector outlooks are positive. There are some common growth drivers in the CIS markets covered in this report. One is the introduction of new categories of compulsory insurance, such as mandatory health and compulsory MTPL insurance in Azerbaijan and Georgia, respectively. Another is the opening of CIS economies. For example, WTO membership should (eventually) help Kazakhstan further open its real economy and financial sector.

Another important factor is regulation. For instance, Kazakhstan has a robust regulatory framework and in Azerbaijan, a new unified system for damage assessment in motor cover should build consumer trust in the insurance sector. On the flipside, an unexpected decision in Georgia to reverse liberalization in healthcare led to a slump in medical premiums in 2014, showing how regulation can also hinder insurance sector growth.

Latin America

Bolivia, Colombia, Ecuador and Peru form Latin America’s largest block of frontier markets. The insurance and sectors in Peru and Colombia are further developed than those in Bolivia Ecuador, mainly due to structural and institutional reforms carried out in the 1990s and early 2000s. The regulatory and operating environments in these markets have improved considerably, and have encouraged foreign insurer participation, increasing their market share in Colombia from 34% in 2003 to 41% in 2014. In contrast, foreign participation in the Bolivian market has practically disappeared, and the business environment in Ecuador has grown more challenging with the worsening economic climate and steady encroachment of the state into the local re/insurance markets.

Southeast Asia

In Southeast Asia, Cambodia, Laos, Myanmar and Vietnam (CLMV) are four of the smaller markets, and they have had significant development in recent years. The CLMV economies have benefited from more stable domestic socio-political environments and further integration into the global economy.

The insurance industry in CLMV is at an early stage of development and is being driven by the non-life sector. Vietnam is the most developed market in the region, and has the highest insurance penetration. The CLMV markets are revising insurance and related regulations to enable faster sector growth. For example, a new Insurance Law in Cambodia took effect from February 2015. In Myanmar, where the insurance market has been in state hands since 1963, twelve private companies were granted conditional approval to provide insurance services in 2013. Two other developments that will potentially act as growth drivers for insurance in CLMV, alongside stronger GDP growth, are the ASEAN Economic Community and China’s One Belt, One Road policy. Both are explored in this sigma.

Figure 1: Frontier markets covered in the sigma report

Source: Swiss Re Economic Research & Consulting.