Global insured losses from catastrophes were USD 45 billion in 2013, Swiss Re sigma says

26 March 2014 | Company News & Results | Swiss Re | Swiss Re

• Total economic losses from natural catastrophes and man-made disasters were USD 140 billion in 2013 • Global insured losses were around USD 45 billion in 2013, with large contributions from flooding and hail events • Around 26 000 lives were lost in natural catastrophes and man-made disasters in 2013 • A special chapter on climate change in the sigma says rising global temperatures are expected to lead to shifts in the frequency, intensity and duration of extreme weather events

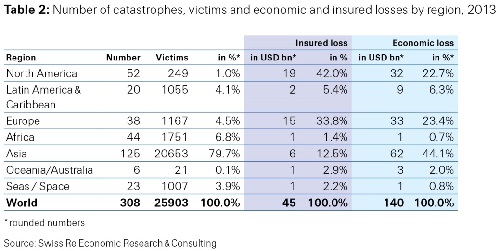

According to the latest sigma study, global insured losses from natural catastrophes and man-made disasters were USD 45 billion in 2013, down from USD 81 billion in 2012. Of the 2013 insured losses, USD 37 billion were generated by natural catastrophes, with hail in Europe and floods in many regions being the main drivers.

Total economic losses from catastrophic events were USD 140 billion, down from USD 196 billion in 2012 and well below the 10-year average of USD 190 billion. The number of victims in disaster events grew to around 26 000 in 2013 from 14 000 the previous year.

Haiyan was the biggest humanitarian catastrophe in 2013

Asia was hardest hit by natural catastrophes in terms of economic losses and victims. Typhoon Haiyan in the Philippines in November brought some of the strongest winds ever recorded, alongside heavy rains and storm surges. Around 7 500 people died or went missing, and more than 4 million were left homeless. The second biggest humanitarian disaster of 2013 was the June flooding in the state of Uttarakhand in India, which claimed some 6 000 lives.

Europe suffered heavy losses in 2013

Europe suffered the two most expensive natural disaster events in 2013. Massive flooding in central and eastern Europe in May/June after four days of heavy rain caused large-scale damage across Germany, the Czech Republic, Hungary and Poland. Total economic losses were USD 16.5 billion, and the insured loss was USD 4.1 billion. Not long after, in late July parts of Germany and France were hit, this time by severe hailstorms. The storms struck heavily populated areas in Germany, which, according to latest estimates, generated most of the entire insured loss total of USD 3.8 billion, the largest ever from a hail event, worldwide.

Many regions around the world were hit by floods in 2013. The single largest loss-event in North America was extensive flooding in the city of Calgary, Alberta and surrounding area following six days of torrential rain. The economic loss was USD 4.7 billion and the insured loss was USD 1.9 billion. Floods also generated losses in Australia, Asia and South America.

Overall, global insured losses were significantly lower in 2013 than in 2012. This was mainly because of a very quiet hurricane season in the US. Nonetheless, with insurance penetration greater than anywhere else, the US still had the biggest insured loss total last year. This was due to several tornado outbreaks and related thunder and winter storms.

Global protection gap continues to widen

Risk prevention and mitigation measures have progressed in recent years. For instance, the losses from the floods in central and eastern Europe last year would have been much worse had the flood protection measures not been strengthened after the same region suffered severe flooding in 2002. Likewise, a very effective pre-designed evacuation drive saved thousands of lives when Cyclone Phailin made landfall in Odisha, India in October, with winds of up to 260 km per hour.

However, the cyclone destroyed around 100 000 homes and more than 1.3 million hectares of cropland. Kurt Karl, Chief Economist at Swiss Re says: "The total economic loss of Cyclone Phailin is estimated to be USD 4.5 billion, with just a tiny portion covered by insurance. The insurance industry can play a much larger role in helping societies deal with the fallout of disaster events, such as this and Typhoon Haiyan."

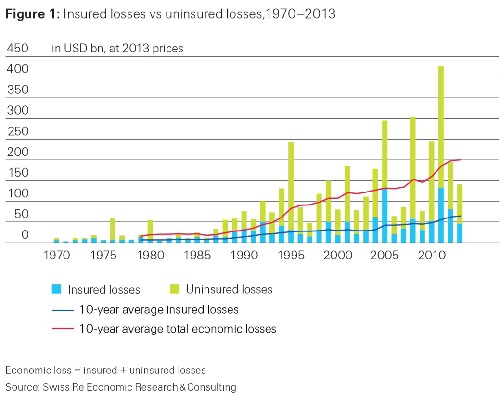

The protection gap, the difference between total losses and insured losses, has progressively widened over the last 40 years. Disaster events continue to generate increasing total losses alongside ongoing economic development, population growth and urbanization.

Fostering climate change resilience

This sigma includes a special chapter on climate change, which is widely acknowledged to be caused by rising greenhouse gas emissions. Industrialization and human activity has led to a significant increase in greenhouse gas emissions which, alongside natural variability, have pushed global temperatures higher.

Rising temperatures are expected to lead to more frequent and severe extreme weather events in the future. If no action to reduce greenhouse gas emissions is taken, these events are likely to become an increasingly important factor in the ongoing upward trend of total losses. As this sigma report shows, along the US Gulf coast, for example, the economic loss potential of climate change may rise to USD 21.5 billion per annum by 2030. However, "a number of cost-efficient adaptation measures are available, and these together could lower damages by 35%," says David Bresch, Global Head Sustainability at Swiss Re.

"Among the most attractive adaptation measures are beach nourishment, levees, roof cover retrofits and improved building codes."

Risk prevention and avoidance, and disaster risk management measures can help build resilience to climate change. So too can risk transfer solutions, by providing financial relief after a disaster has struck. Risk transfer does not stand in isolation: it is an integral part of any climate adaptation strategy.