Global insurance premiums increased in 2016 and overall growth outlook remains positive, latest Swiss Re Institute sigma study says

• Global insurance premiums increased by 3.1% in 2016; down from 4.3% growth in 2015. • Life premium growth slowed to 2.5% and non-life to 3.7% in 2016, due to weaker performance in advanced markets • Profitability in the life and non-life sectors weakened amid low interest rates and robust competition • Life and non-life premiums in China grew very strongly, but many other emerging markets were in slowdown mode • Emerging markets to continue to drive global premium growth; stronger activity in advanced economies to boost non-life sector • Special chapter says digital distribution in insurance is growing, but agents and brokers will continue to play an important role

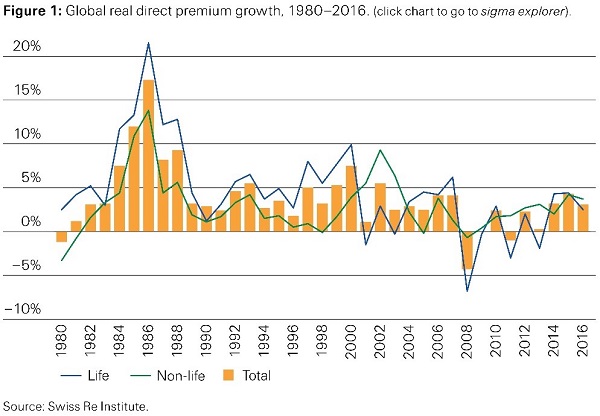

Global insurance premiums increased by 3.1% in real terms in 2016, a fairly solid outcome in an environment of moderate global economic growth, Swiss Re Institute's latest sigma report says. The main cause of the weaker global premium development compared to 2015 were the advanced economies but growth in many emerging markets – excluding China – slowed also. Global life premium growth slowed to 2.5% in 2016 from 4.4% in 2015 as advanced market premiums contracted, while life premiums in the emerging regions together grew by more than double the long-term average. On the non-life side, global premiums grew 3.7% in 2016, reflecting relatively solid expansion among the emerging countries and another exceptional performance in China. The emerging markets will likely fuel improvement in life premiums in the coming years, with China and India being the main growth drivers. Non-life premium growth is expected to remain moderate, with stronger economic activity in the advanced markets supporting momentum.

Total direct insurance premiums written grew by 3.1% in real terms in 2016, down from 4.3% growth in 2015. The increase in 2016 came despite global economic growth – a key driver of insurance demand – of just 2.5%. In nominal USD terms, global insurance premiums were up 2.9%. Nominal growth was lower than real due to currency depreciations, particularly in the UK and some emerging countries.

The China growth engine steams ahead, in life and non-life sectors

Global direct life insurance premiums totalled USD 2 617 billion in 2016, up 2.5% in real terms. This was slower than the 4.4% expansion in 2015 but still above the 10-year average of 1.1% growth. Emerging markets remained the main source of global growth, with premiums up 17%, more than twice the 10-year average of 8.4%, and primarily driven by rapid growth in China. "The life sector in China is growing very rapidly," says Kurt Karl, Chief Economist at Swiss Re. "Sales of traditional life products were very strong in 2016, benefitting from further liberalisation of interest rates and government efforts to encourage growth of protection products."

Excluding China, overall emerging market life premium growth was significantly lower but still a hearty 5.7%, driven by gains in India, Indonesia and Vietnam. It was a different story in the advanced markets, where premiums contracted by 0.5% in 2016, extending a 10-year period of stagnation in premium development.

In non-life, global premiums grew by 3.7% in 2016, down from the 4.2% gain in 2015 but more than the 10-year average of 2.0%. Once again, premium growth in the emerging markets was solid at 9.6%, above the 10-year average of 8.3%. However, the emerging market outcome was heavily skewed by China, where non-life premiums were up 20%.

A surge in demand for health insurance and sustained but slowing demand in motor insurance underpinned non-life premiums in China. Excluding China, emerging market premiums overall increased by just 1.7%. Non-life premium growth in the advanced markets slowed to 2.3% in 2016 (2015: 3.3%), but that was well above the 10-year average of 1.0%. Growth weakened in all major advanced regions (except Oceania) due to lower economic growth and softer rates.

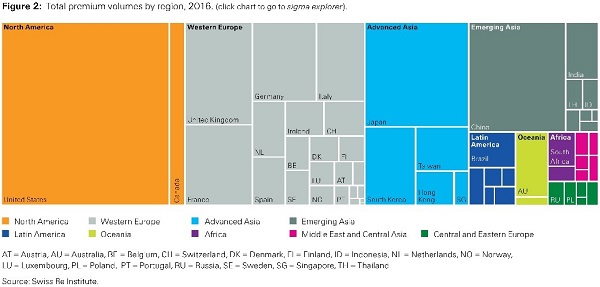

China is the world's number three insurance market

In 2000, China was the 16th largest market globally in terms of total insurance premiums written. By 2016, it was the world's third largest market with USD 466 billion in total premiums, not much smaller than the second largest market, Japan (USD 471 billion), but still much smaller than the US (USD 1.35 trillion). The interactive infographic below tracks China's development to its position as world number 3, which it has held since 2015.

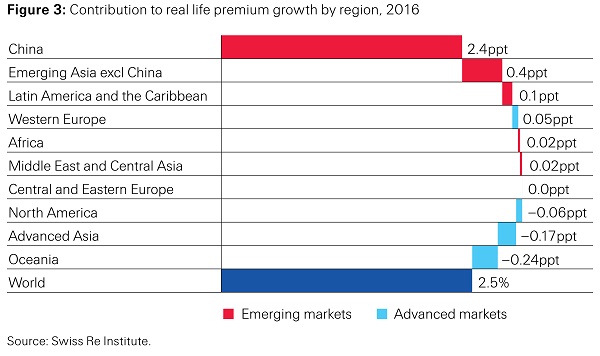

In life insurance, China was the most important source of premium growth in 2016. It contributed 2.4 percentage points (ppt) of the global 2.5% growth in sector premiums last year. All other markets combined were responsible for the remaining 0.1 ppt (see Figure 3). In non-life, regional/country contributions were more balanced. For example, despite much stronger premium growth rates in China in 2016, the advanced markets continued to play a major role in the global market. Together, North America and Western Europe contributed 1.8 ppt of the 3.7% growth in global sector, and China 1.7 ppt.

Low interest rates continue to pressure profits

With still low interest rates, profitability in the insurance industry remains under pressure, and return on equity (ROE) declined in both sectors in 2016. In life, moderate premium growth in many markets also dragged on profitability, while the non-life sector was further impacted by lower underwriting results. In the US, the non-life sector experienced its first underwriting loss in four years, driven by higher catastrophe losses and lower releases from prior-year loss reserves. Despite pressure on profits, however, both the life and non-life insurance sectors remain well capitalised.

Premium growth likely to improve, but profits to remain under pressure

Global life premium growth is expected to improve in the coming years, mainly driven by the emerging markets, in particular China and India. Advanced markets should also grow, but only moderately. While North America is expected to outperform Western Europe, growth will likely be highest in advanced Asia. Growth in global non-life is expected to remain moderate, with stronger activity in the advanced economies lending support. Premium growth is expected to improve in North America and advanced Asia, but remain flat in Western Europe and Oceania. Emerging markets are likely to grow robustly but at a slower pace than in the recent past. There will be healthy growth in China and to a lesser extent in India.

Managing legacy savings business with embedded guarantees will remain a major challenge for life insurers' profitability in the coming years. Historically-low interest rates are likely to persist and limit the ability to offer attractive savings products to boost new business. Life insurers will continue to re-orientate their business models and shift their focus from traditional savings to life protection products, but it will be a while before these measures have an impact. The profitability of non-life insurers is expected to remain pressured given still-low investment returns, and as underwriting results are impacted by the continued soft market conditions and dwindling reserve releases.

Digital distribution continues to grow; intermediaries are here to stay

This sigma includes a special chapter on developments in digital distribution in insurance. There has been a proliferation of direct digital distribution channels in recent years, in some markets. At the same time, the share of traditionally intermediated insurance business remains dominant globally. The digitalisation of insurance distribution is set to continue, but the pace of change will vary across markets. Digital channels will ultimately be used throughout the distribution process, from information gathering to purchase completion to after-sales service. But not all insurance transactions will migrate to online, and intermediaries will continue to play an important role.