Global economic growth is solid but slowing, and emerging Asia will continue to power the insurance market, sigma says

- Global economic growth will remain solid over 2019/20, but momentum has peaked and downside risks have increased

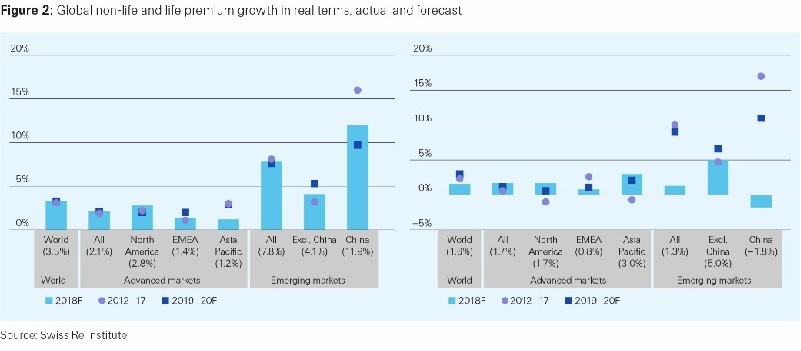

- Global premiums are forecast to grow by around 3% annually in 2019 and 2020, and in emerging Asia by three times more

- The economic power shift from west to east will drive insurance sector development to 2020 and beyond

- Expanding the boundaries of insurability for corporate intangible assets will be another main growth area for insurers

- A newly-estimated USD 500 billion global property and mortality protection gap signals the large opportunity for insurers to help improve resilience

Global economic growth will remain strong over the next two years, although momentum has peaked. Swiss Re Institute's latest sigma "Global economic and insurance outlook 2020" says the still-positive economic momentum will support the insurance sector, with global premiums up more than 3% annually over the next two years in real terms, a one-percentage point increase from 2018. Most demand will come from emerging Asia, where premiums are forecast to increase at more than three times the global average rate, by close to 9%. Innovation in insurance will expand the boundaries of insurability and further drive premium growth. It will also help improve global resilience by narrowing existing insurance protection gaps.

"The global economy has been performing well, and growth will remain solid," says Jérôme Jean Haegeli, Chief Economist at Swiss Re. "However, the best is probably over. Cyclical momentum is positive but we expect real GDP to slow by about 1-2 percentage points in most parts of the world over the next two years. This also takes into account mounting structural challenges to growth, such as higher debt burdens, reduced savings on account of aging societies, and low productivity."

Swiss Re Institute estimates that the US economy will grow by 2.9% growth in real terms in 2018, and by 2.2% in 2019 (consensus 2.6%1) and 1.7% in 2020 (consensus 1.8%), as the Federal Reserve becomes less supportive and fiscal stimulus fades. Growth in the Euro area is forecast to slow to 1.5% and 1.4% in 2019 and 2020, respectively, from 1.9%. For Japan, GDP growth of 0.6% is forecast next year, down from 1.0% in 2018, due to weaker external demand.

The emerging markets, particularly in Asia, will continue to grow. Aggregate emerging market growth is expected to strengthen to around 4.9% annually over 2019 and 2020, after a 4.7%-gain this year. The forecasts are based on anticipation of economic recovery in countries that have struggled in recent years, including Argentina, Brazil, South Africa and Turkey. Emerging Asia will continue to outperform, with the Chinese and Indian economies forecast to grow by more than 6.0% annually over the next two years.

Downside risks increase

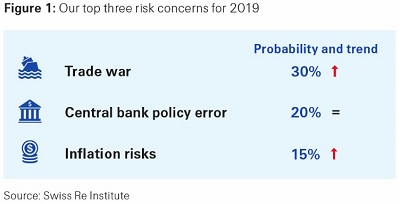

Downside risks to global growth have increased of late. In the medium term, the record low level of unemployment in the US will likely lead to higher wage gains, and higher risk of overheating in the US. This could disrupt the expected trajectory of monetary policy normalisation, with the Federal Reserve raising rates more aggressively than expected. Excessive tightening of financial conditions would lead to greater market volatility and a slowdown in economic activity. Longer term, the main risk is escalation of current trade tensions between the US and China into a global trade war. The report estimates that in a worst case scenario such as a 10% tariff on all goods trade worldwide, global GDP would reduce by 1.5%-2.5% over three years.

From west to east: emerging markets to drive insurance growth

Insurance premium development will be supported by the solid economic growth environment. Swiss Re Institute forecasts that global non-life and life premiums will both grow by around 3% annually over 2019/20. The gains will be driven by the emerging markets. Wealth in the emerging markets has grown significantly and a 1-percentage-point rise in GDP 2018 has a much greater impact in premium volume terms than it would have had a decade ago.

In addition, many markets have progressed to the steeper area of the insurance "S-curve" and the impact of income growth on insurance demand is much bigger.

"With the global economic power shift from west to east continuing unabated, China and emerging Asia in particular, will be the main source of insurance demand in the coming years," Haegeli says. "Based on our models, we project that in US dollar terms, the growth rate of insurance premiums in emerging Asia will be more than three times that of the world average over the next two years." According to sigma data, China's share of global premiums increased from 0.8% 2000 to 9.7% in 2017, and is forecast to expand to 16% by 2028.

Ten years after the global financial crisis, is the world more resilient?

The latest sigma also addresses the issue of resilience, saying that the world economy remains ill-prepared for a global recession. The economy has less capacity to absorb shocks given the lower growth trends when compared to 10 years ago, higher debt burdens, weaker financial market structures and a move to less openness. Swiss Re Institute encourages a move towards more private capital market solutions to remedy the situation, with the public sector promoting financial market standards wherever possible (for example for sustainable and infrastructure investments), state contingent debt instruments for sovereigns, further country-specific structural reforms and less central bank intervention.

Insurance is a central pillar of resilience and with a more-supportive policy environment, insurers will be better able to expand their risk-absorbing capacity and long-term investment activities in resilience-building projects such as infrastructure. According to latest data from different sources, this sigma estimates that the global re/insurance sector has total assets under management of about USD 30 trillion – roughly three times the size of China's economy. This large asset base should be fully mobilised as risk absorber. Further, the report newly estimates that the global mortality and property protection gap currently stands at USD 500 billion in premium-equivalent terms. The gap represents the still elevated vulnerability to adverse events for many households and businesses across the world, and the very large opportunity for insurers to further contribute to improving resilience.

Innovation in insurance will narrow protection gaps. Product innovations such as parametric insurance, for example, are expanding the scope of insurability for natural catastrophe risks that have previously been difficult to insure. Technology will support the innovation. For example, businesses are seeking covers for previously uninsurable exposures like earnings and cash flow losses due to contingent business interruption, cyber, product recall and weather and energy price risks. The evolution of double-trigger indemnity structures, and data and modelling advances is allowing insurers to develop ever-more innovative covers for such exposures.

The full report can be downloaded here.