Demand for customised reinsurance and insurance solutions is growing, Swiss Re sigma says

* There is increasing demand for customised and more strategically-motivated re/insurance solutions

* Structured solutions increase efficiency of risk protection programmes compared to standard products

* Reinsurance can also be used as a corporate finance tool and to support a cedent's long-term growth ambitions

* Key factors for success include a clear objective, experience, capacity, use of best practices and transparent communication

The latest sigma study "Strategic reinsurance and insurance: the increasing trend of customised solutions" focuses on the utility and rising use of non-traditional re/insurance solutions. Strategic reinsurance programs are designed to provide more efficient risk protection and can help insurers optimise their capital structure in order to improve capital returns and minimise capital costs. Hence, insurers increasingly integrate reinsurance into their long-term strategy and growth plans. Strategic solutions are also used to manage challenging circumstances, such as mergers and acquisitions, changes in regulatory regimes, or market dislocations.

Insurers and large corporations have become more sophisticated in managing their capital and risks, often centralising re/insurance buying across lines of business and territories. The development has been driven by insurance industry consolidation, globalisation of risks, technological innovations, and regulatory reforms. "This has led to higher limits and higher retentions, as well as the substitution of local contracts with larger and more complex solutions", says Swiss Re Chief Economist Kurt Karl. "However, this goes hand-in-hand with a greater need for tailored re/insurance structures that address unique situations and can sometimes be enhanced with innovative features to meet specific client needs."

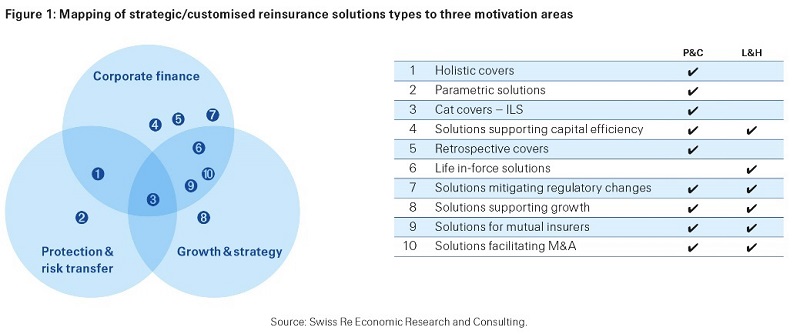

Three motivation areas

Strategic solutions represent a growing area of demand in the industry. Transfer of risk is a fundamental premise of any re/insurance transaction, including customised solutions. However, the rationale for the use of such solutions has evolved into three broader motivation areas. The first is structured solutions, designed to increase the efficiency of re/insurance by combining multiple risks and/or interdependent triggers.

part of a more integrated risk management process, risk transfer is focused on the joint distribution of all risks, helping to expand the insurability of difficult-to-insure risks. It can also provide large amounts of capacity for catastrophe risks, the latter a challenge for some smaller re/insurance carriers in particular.

The benefits of a risk transfer program can be demonstrated by a recent case of a state-owned power utility in Uruguay purchasing combined insurance protection against drought and high oil prices. Pay-outs would be triggered when rainfall levels moved below a trigger level, with higher payments when the price of oil was high. The index-based insurance solution protected the utility against earnings volatility and, ultimately, consumers against the risk of high electricity prices.

Customised reinsurance solutions also offer risk transfer benefits to ceding insurers. For example, a small regional insurer in the US was subject to volatile losses resulting from severe convective storms. It needed protection against earnings volatility, not least so that it could maintain its credit rating. The solution was a multi-year reinsurance program with profit sharing and cancellation features which gave the insurer the benefit of long-term capacity at consistent pricing levels.

The second non-traditional use of reinsurance is for corporate finance purposes, that is, to address capital management issues. Cost-of-capital and capital efficiency have become increasingly important in the current and ongoing low-yield, low-growth environment, and reinsurance can substitute traditional capital and boost profitability. Corporate finance-oriented solutions include non-life retrospective covers and life inforce monetisation with the goal of releasing trapped capital and monetising future expected cash flows on long-term business.

The third motivation for the use of customised reinsurance solutions is to enable the strategic and long-term growth objectives of a ceding insurer. In the life sector, reinsurance contracts can be geared toward helping an insurer fund the high expenses and negative cash flows associated with growth of new business. In non-life, growth support via reinsurance is more focused on flexible, on-demand capital relief and on improving capital efficiency. The cedent can also benefit from a reinsurer’s technical and market expertise.

The three motivation areas for the purchase of strategic re/insurance are not mutually exclusive. For example, large catastrophe programs may straddle all three. Figure 1 lists 10 possible applications of non-traditional solutions, and how these map to the three motivation areas.

The reinsurance solutions toolbox includes many concepts that can be modified and combined to address the needs of a client. There are as many forms of bespoke solution as there are client situations. This sigma uses case studies to demonstrate the 10 applications of customised solutions listed in Figure 1, and the resulting benefits.

Strategies for success

The use of customised structures as tools for achieving longer term corporate finance and strategic goals is often a multi-year process. In all instances, successful transactions are based on close alignment among all stakeholders, which can include insurer, reinsurer, broker and regulator. A number of factors contribute to a successful strategic reinsurance agreement, including clear objectives, senior executive sponsorship within the cedent, experienced deal teams, large risk capacity, long-term relationships, and best-practice accounting, tax and regulatory compliance. Lastly, transparent communication among all stakeholders in a transaction is critical.