PPS expands its disability benefits with functional disability cover

To truly be the leader in the graduate professional market we need to ensure we have a broad range of benefits available to cover all the diverse needs of PPS members. We are proud to say that PPS members can now obtain disability cover, irrespective of their occupation, with the launch of the new PPS Functional Disability provider.

What does this enhancement entail?

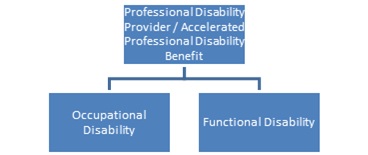

The Functional Disability provider is a new option available under the PPS Professional Disability Provider or Accelerated Professional Disability Benefit. These products will now offer two options to cover disability-related conditions and the impact thereof:

• The first is the (existing) Occupational Disability provider, that pays out 100% of the benefit should the life-insured become occupationally disabled.

• The second is the (new) Functional Disability provider, that pays out a lump sum benefit if the life-insured suffers from any of the listed functional disability events. The payout amount will be based on the severity of the condition and may be 25%, 50%, 75% or 100% of the insured amount.

Members can choose to be covered for either, or both functional disability and occupational disability. Functional disability focuses on conditions that will have an impact on the member’s ability to function, whereas occupational disability focuses on conditions that will render a member unable to do his/her occupation. Note that members will benefit from the overlap between medical events that may lead to both loss of function and the inability to work, through our provision of the SYNC discount, activated when members decide to buy both occupational and functional disability benefits.

What makes the PPS functional disability offering different?

• Functional disability uses medically defined definitions to ensure members are assessed objectively.

o It is more lenient, realistic and comprehensive compared to other functional impairment benefits in the market. For example:

Organ transplants are covered when the member is on a waiting list, not only after the procedure is completed and unsuccessful.

Psychiatric conditions do not require permanent institutionalisation before the benefit may be claimed.

o It uses a scoring model to determine the level at which a payment will be made. This allows for a successful claim where a condition results in multiple mild impairments (instead of a single significant one).

• Functional disability allows for multiple claims which is especially important for progressive conditions like renal failure.

• When members choose to be covered for both occupational disability and functional disability:

o They will receive the SYNC discount, reducing the member’s total premium for the benefit.

o Claims will first be assessed for occupational disability, and if the claim does not qualify for a benefit, it will then be assessed further under the functional disability definitions.

Do members need this type of cover?

According to our research, 82.5% of lump sum disability products sold to professionals across the insurance industry, consist of both occupational disability and functional disability definitions. Clients clearly value the comprehensive protection they will enjoy by holding both types of benefits. Thus, new members will find value in taking out both, and existing members in adding functional disability to their existing lump sum disability cover.

Looking at the broader picture for disability-, functional- or critical illness cover, each product offering solves for a component of the broader needs of a member, so this is also a great opportunity to make sure other benefits fulfil their respective purposes as well.