MMI Holdings Trading Update

Trading update for the three months ended 30 September 2015

Operational overview

• The MMI group continued to attract new single premium inflows, ending 3% higher than the very strong prior year comparative quarter with Momentum Retail, Metropolitan Retail and International all contributing strongly.

• New business recurring premiums were lower than the same quarter of 2014, mainly held back by lower Corporate and Public Sector sales and the distribution restructuring that is taking place in Metropolitan Retail.

• Satisfactory client retention was experienced across the group.

• The growth in the market value of investment assets under management has been curtailed by the performance of markets as a whole, resulting in pressure on top-line asset-based fee income in the current year.

• Good expense management across the group in MMI’s established operations, on the other hand, is contributing positively.

• MMI continues to invest in strategic growth initiatives in line with the group’s strategy, including the middle market, International, Investments and Momentum Short-term Insurance businesses, to achieve long-term goals.

• MMI is successfully implementing its client-centric strategy.

• Good progress has been made with the Product and Solutions Centres of Excellence under the client-centric operating model, enabling related optimisation opportunities.

Operating environment

• Growth in the South African economy has continued to slow down and this is putting substantial pressure on the disposable income of our clients.

• Equity market volatility continued with the JSE all-share index falling about 3% during the quarter.

• According to the Momentum / UNISA South African Wealth Index, South Africa households’ net wealth decreased in real terms in the second quarter of 2015.

• There are, however, still opportunities for MMI in the various market segments as identified by the client-centric focussed distribution teams.

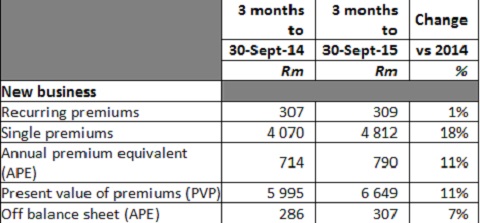

Momentum Retail

• Overall Momentum Retail delivered pleasing new business growth.

• New recurring risk premiums were positive compared to the prior quarter while savings premiums reduced slightly.

• Strong single premium new business growth continued, ending 18% above the prior quarter’s total.

• New business volumes (PVP) for the quarter ended 11% higher than those recorded in the prior year.

• The mix of new business continues to favour single premium investments.

• Steady progress is being made with developing new client-value propositions.

• Mortality experience profits during the quarter were below our longer-term expectations.

• Client service and retention remained at satisfactory levels.

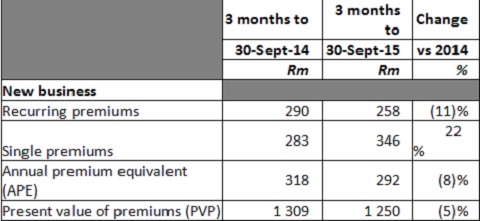

Metropolitan Retail

• Single premium income once again performed very well, increasing by 22% over the prior quarter.

• Recurring premium new business continues to be impacted by the distribution model changes implemented earlier this year, however there is noted progress with the performance in the current quarter exceeding that of the last two quarters of the previous financial year.

• Persistency is monitored closely, especially in light of the tough market conditions. It is therefore pleasing that it has improved slightly during the quarter and remains better than the targeted range.

• Overall the distribution model changes are having a positive impact on the business and the productivity per agent has started increasing. Further new business improvements are expected over the next three quarters.

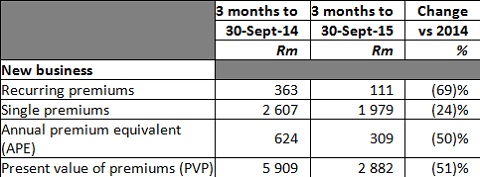

Corporate and Public Sector

• After a very strong performance during the year to June 2015 both risk and investment recurring premium new business slowed down during this quarter.

• Single premium levels remained solid, with retirement funds and investments doing well when compared against an excellent quarter in 2015. The current performance is still one of the top three quarters recorded over the past four years. This business is traditionally lumpy in nature.

• Securing new business in the group insurance and investment markets remains highly competitive.

• A new business pipeline of potential opportunities has been identified and is being actively pursued.

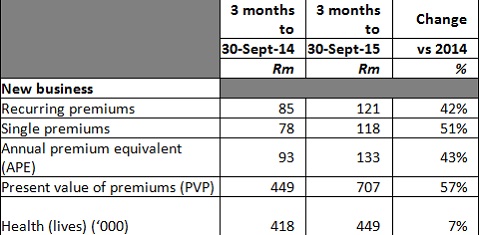

International

• International continued to deliver strong new business growth.

• Good new business volumes were recorded in almost all the life insurance operations during the period under review.

• Strong growth was experienced in Namibia through the new combined product range.

• The medical claims ratio has deteriorated slightly when compared with the prior year, putting pressure on profitability in the health businesses.

• The good growth in members under health-care administration continued.

• MMI is increasing its stake in the Indian joint Venture to 49%. Good progress has been made in submitting the required regulatory applications.

Products and solutions – Centres of excellence

Investments and savings

• Aluwani Capital Partners, the new BEE asset manager announced to the market in September 2015, has obtained an asset management licence and will commence trading in December 2015.

• Implementation of the partnership with RMI, as disclosed with the year-end results, has continued to make good progress.

• The longer-term outlook for the Investment and Savings Centre of Excellence remains positive as the alignment with the outcomes-based investment strategy is strengthened.

Health

• The various health businesses within MMI have aligned as a Centre of Excellence under a single strategy.

• Good progress has been made with optimising the restricted scheme administration business in anticipation of the departure of two administration contracts, in January 2016, as disclosed as part of the 2015 year-end results announcement.

• The business continues to submit tenders when opportunities arise and MMI is pleased that the health business has recently managed to secure some new contracts.

• The growth in the number of members in the Momentum Health open scheme continued during the quarter.

Short-term insurance

• New business growth has slowed as Momentum Short-term Insurance continues to implement process and pricing improvements.

• Premiums for the quarter grew year-on-year by 34%, with an improvement in the quality of business written through changing the channel mix and repricing new business.

• The claims ratio for the quarter improved to 87%, but remains above the longer-term target.

Kagiso Tiso Holdings (KTH) / MMI preference shares

• KTH requested that a further 1.0 million of the A3 preference shares be converted into ordinary shares. These converted shares were listed on 5 October 2015.

MMI subordinated debt

• MMI issued R1 000 million of subordinated debt in September 2006 with a first-call date of September 2015.

• In line with the original intention and timeline MMI redeemed this debt during September 2015.

AGM

• The MMI AGM was held on 20 November 2015 and all resolutions tabled were passed with the required majority of votes.

Comments / qualifications

• All figures are provisional and unaudited, and are for the period 1 July to 30 September for all years presented as reported in the current internal management accounts.

• The basis on which the new business figures have been calculated is the same as that used for embedded value purposes. Premium income is included from the date on which policies come into force as opposed to the date on which they are accepted.

• The new business figures are all net of outside shareholder interests.

• The current disclosure reflects the new client-centric operating model. Where appropriate certain prior year comparatives have been adjusted to reflect the new structure.