Liberty's claim statistics show a significant increase in retrenchment and mortality

Liberty's claim statistics for 2020 show a significant increase in retrenchment and mortality claims following the beginning of the COVID-19 pandemic and hard lockdown in April, which had a substantial impact on the country's economy.

In 2020 Liberty paid out R6.34 billion in claims to its individual clients under the flagship Lifestyle Protector product and legacy risk products. This is an increase of 7.64 percent compared to 2019 claims, which is broadly in line with average yearly increases over the past decade.

The group paid out a total of R12.4 billion in claims to its clients across its retail business, corporate business, emerging consumer market, direct financial services business and business sold through Standard Bank channels.

Retrenchment claims

Retrenchment claims peaked between August and October in 2020 on the back of a lag effect from the start of lockdown. During these three months, retrenchment claims peaked at over 60 per month, compared to just over 10 per month during January and February in the same year, showing the effects of the economic contraction at the start of the pandemic.

"This trend was expected given the harsh realities and subsequent impact on jobs because of the pandemic. The most impacted regions were, not surprisingly, the main economic hubs of Gauteng, the Western Cape and KZN," says Kresantha Pillay, head of Liberty's flagship Lifestyle Protector solution.

Mortality claims

Also, during the peak of the first wave of the COVID-19 pandemic between June and September 2020, Liberty saw a substantial spike in mortality claims of around 200 percent, or three times, above normal levels.

"It is important to note of course that claim statistics in 2020 reflect only the effects of the first wave of COVID-19 in the middle of the year," Pillay says.

COVID related claims

According to Nalen Naidoo, Liberty's Divisional Executive for Retail Risk Propositions, the group had set in motion a series of emergency plans to deal with the surge as the full extent of the pandemic became clear.

Over half a billion rand (R575 million) was paid out to cover confirmed COVID-related death and health-related claims, of which death was the leading cause. COVID-19 related funeral claims peaked during the first wave with most claims coming from the Eastern Cape, Gauteng and the Free State.

"These COVID-related claim statistics are based on available medical data during the pandemic. Because of the variability in official medical reporting of COVID deaths, attributing some natural causes* claims to COVID was a challenge for us, and we estimate that we paid out much more than the R575 million," adds Naidoo.

Overall claims

Despite the pandemic, in terms of impairment and death claims from Liberty's Lifestyle Protector products, death and impairment by cancer and leukemia was the top reason for claims, representing 27 percent. This was followed by cardiac and cardio-vascular-related causes, comprising 20 percent of all claims. These top two causes are unchanged from 2019.

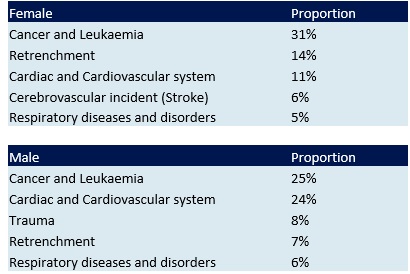

Gender claims and cancer

A breakdown in terms of gender showed similarities in terms of claims. Cancer and leukemia remained the leading cause of impairment and death, but cardiac and cardio-vascular-related causes played a higher relative role for men than women.

Liberty's statistics show that in terms of cancer, prostate cancer is still the leading cause of claims among men, while for women, it is breast cancer.

"Cancer remains a major cause for claims and this has been a trend over the years. The prevalence of particular types of cancer in South African society remain evident," says Liberty's Chief Medical Officer, Dr Dominique Stott.

The long-term psychological effects of COVID

Psychiatrist Dr Ingrid Williamson says that the long-term effects of COVID-19 are being recognised as a growing problem.

Many of those hospitalised for COVID-19 are not able to return to their former level of functioning and require ongoing health care.

**Findings from patients showed that 34 percent had been diagnosed with neurological or psychiatric symptoms within six months of their acute infection, of which 12.8 percent were diagnosed for the first time with such a disorder, mostly depression and anxiety.

These disorders are significantly more common in COVID-19 patients in comparison to groups of people who have recovered from flu and other respiratory conditions.

"Due to the debilitating nature of this disease, specific psychiatric disorders post COVID-19 symptoms such as depression, anxiety, PTSD, dementia and psychosis have been a real phenomenon, and this has an impact on the wellbeing of a lot of people," she says.

"Life and disability cover benefits therefore become very important in times such as these," adds Dr Stott.

Caring for clients during COVID

Liberty also paid R111 million in ADDLIB Bonus payouts, which is a benefit to qualifying clients to receive a cash-back on their premiums under the Lifestyle Protector product suite. This pay-out came at a time when clients needed some financial injection to help them navigate this tough period.

"The pandemic also presented an opportunity for us to learn more and to improve our processes to serve our clients better. This included the acceleration of digitization across the board to evolve the claims experience for our clients," says Naidoo.

At the beginning of the pandemic, it was industry wide practice to add COVID exclusionary clauses to risk policies. However, Liberty made a business decision to remove all COVID-related exclusion clauses at the underwriting and claims stage across all of its risk policies.

"We at Liberty paid out all valid claims to our clients for the benefits they were covered for, irrespective of whether or not it was a COVID-19 related condition that was involved.

"It is in these times that the true value of insurance becomes evident. This is a time of major disruption for everyone, and at Liberty we remain even more committed to deliver on our promises and to assist our clients in their time of greatest human vulnerability," Naidoo says.

Click here to read more...