Zurich reports business operating profit of USD 2.9 billion in 2015 and proposes dividend of CHF 17 per share

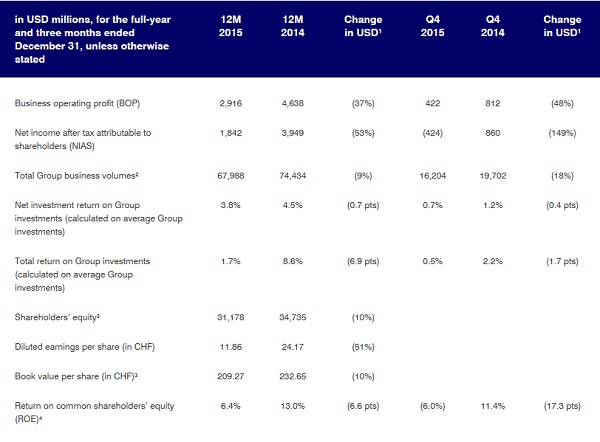

Zurich Insurance Group (Zurich) today reported a business operating profit (BOP) of USD 2.9 billion and net income attributable to shareholders of USD 1.8 billion for the full-year ended December 31, 2015.

• BOP of USD 2.9 billion, down 37% compared with prior year

• NIAS of USD 1.8 billion, down 53% compared with prior year

• BOPAT ROE of 6.4%, down from 11.2% in 2014

• General Insurance combined ratio of 103.6%; ongoing actions underway to restore profitability

• Global Life and Farmers perform well and continue to make progress in strategic execution

• Full-year cash remittances of USD 3.9 billion and strong capital position underpin Board proposal for an unchanged dividend of CHF 17 per share

• Mario Greco to join as Zurich CEO on March 7, 2016

Select financial highlights – full year and fourth quarter (Q4) of 2015

(For a more comprehensive set of financial highlights covering the 12 months ended December 31, see further down)

Chairman and Chief Executive Officer ad interim Tom de Swaan said: “This is a disappointing result, reflecting the previously announced challenges in our General Insurance business and restructuring charges, and we have taken rigorous actions to improve profitability. This includes re-underwriting or exiting unprofitable portfolios, increasing cost efficiency and further simplifying the organization. The remainder of the Group continues to perform well, with both Global Life and Farmers making further progress in the execution of their strategies.”

“Given the challenges within General Insurance, it is unlikely that the Group will achieve its target of a business operating profit after tax return on equity of 12-14% in 2016. Nevertheless, Zurich is on track to achieve its other targets for 2014 to 2016. The Zurich Economic Capital Model ratio stood at 114% as at the end of September, within our target range, and the Group expects to deliver cash remittances in excess of USD 10 billion for the period, well ahead of our target.”

“Given the Group’s healthy cash generation and the strong capital position the Board proposes an unchanged dividend of CHF 17 per share. The Board has also concluded that it is important to maintain the Group's capital strength and flexibility in the current circumstances and has, therefore, decided not to return additional capital to investors at this time.”

“We have accelerated our efficiency program and now aim to exceed the previously communicated cost savings target for 2016 of USD 300 million, and are on our way to achieving group-wide cost savings of more than USD 1 billion by the end of 2018. These savings will be achieved through the application of new technology, lean processes and the offshoring and near shoring of some activities. We estimate that as a result of these necessary measures around 8000 roles across Zurich will be affected by the end of 2018. This figure includes initiatives completed or announced in 2015.”

“Our key priorities in 2016 will be turning around our General Insurance business and continuing actions to position the Group for 2017 and beyond, including enhancing efficiency and sharpening the Group’s retail footprint. We have an excellent management team in place that will be further strengthened with the arrival of Mario Greco, who will lead preparations for the new strategic cycle.”

Segment performance

(for the year ended December 31, 2015)

General Insurance

General Insurance BOP fell by USD 2.1 billion to USD 864 million, 71% in U.S. dollar terms or 70% in local currency terms, as the business recorded an operating loss of USD 120 million in the fourth quarter. The combined ratio deteriorated 6.7 percentage points to 103.6%.

The result was partly due to large losses and natural catastrophe claims, including severe flooding in the UK and Ireland in December and USD 275 million related to the explosions in the port of Tianjin in August. As reported with third quarter results, the business also identified issues in areas such as U.S. auto-liability, Global Corporate property and North America Commercial construction liability. These are being urgently addressed, with targeted measures to reduce earnings volatility and re-underwrite or exit under-performing portfolios.

Gross written premiums and policy fees fell by USD 2.3 billion to USD 34.0 billion, but were up 3% on a local currency basis. This reflected organic growth and an increase in new business through captives in North America Commercial, an increase in premiums in Latin America due to inflation and a new distribution agreement in Brazil. Global Corporate’s gross written premiums and policy fees were broadly similar to the prior year. EMEA was slightly lower in local currency terms, but adjusting for the sale of the retail market business in Russia in 2014 and the exit of a business in the Netherlands in 2015, premium volumes increased.

The business continued to make progress in key areas of its strategy. Successes include the return to profitability of the South African business, and measures to improve the geographic footprint of General Insurance and focus on profitable lines of business. This includes the decision in November to stop writing new general insurance business for retail and commercial customers in the Middle East and exit those lines by the end of 2016 or as soon as possible thereafter.

Global Life

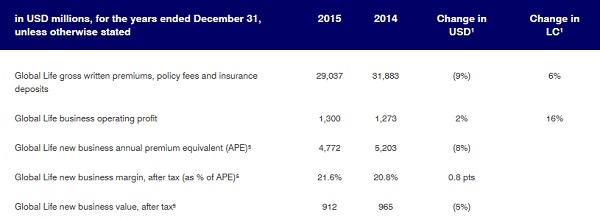

Global Life BOP was USD 1.3 billion, up 2% in U.S. dollar terms or 16% on a local currency basis, as the relative strength of the U.S. currency masked improved operating profits in all markets. Gross written premiums, policy fees and insurance deposits fell by USD 2.8 billion to USD 29.0 billion, or 9% in U.S. dollar terms, but rose 6% in local currency, in part due to increased sales of individual savings products in Italy and Spain, and of protection products through Zurich Santander in Latin America.

Bank joint ventures continued to show steady growth throughout the year and Global Life has already achieved its 2016 goal of a run-rate improvement in BOP of more than USD 80 million from in-force management initiatives.

Structural actions such as the sale of Seven Investment Management and the UK annuities book to Rothesay Life have helped to generate cash remittances of USD 900 million, well ahead of expectation. In addition, Global Life closed its Singapore business to new customers in December.

Farmers

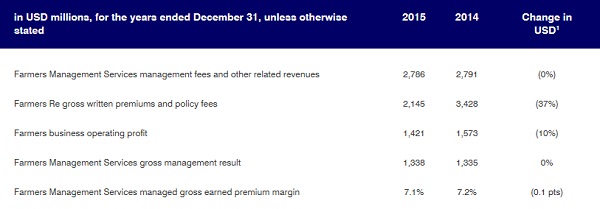

Farmers BOP declined 10% to USD 1.4 billion, largely due to underwriting losses in Farmers Re and lower participation in the reinsurance agreements with the Farmers Exchanges6. Farmers Management Services’ business operating profit fell by USD 23 million to USD 1.4 billion, primarily due to an unfavorable fluctuation in the mark-to-market valuation of certain employee benefits and the gain on the sale of the former headquarter buildings in the prior year.

An increase in auto claims costs across the industry negatively affected the combined ratio of both the Farmers Exchanges and Farmers Re.

Despite these challenges, Farmers Exchanges have continued to make good progress in the execution of their strategy, with improved customer satisfaction and retention rates. The Farmers Exchanges also saw continued growth in their agency network, which increased by around 300 agents to 13,500.

The Non-Core Businesses, which comprise run-off portfolios that are managed with the intention of proactively reducing risk and releasing capital, reported a business operating profit of USD 51 million, compared to a loss of USD 227 million in the prior year. This is largely due to the release of long-term reserves due to a product-related buy-back program and more favorable reserves adjustments than in the prior year.

In Other Operating Businesses, the holding and financing business operating loss fell by USD 240 million to USD 720 million, primarily due to lower interest expenses on debt refinanced in 2014 and 2015, currency gains and lower operating losses from the Group’s headquarters.

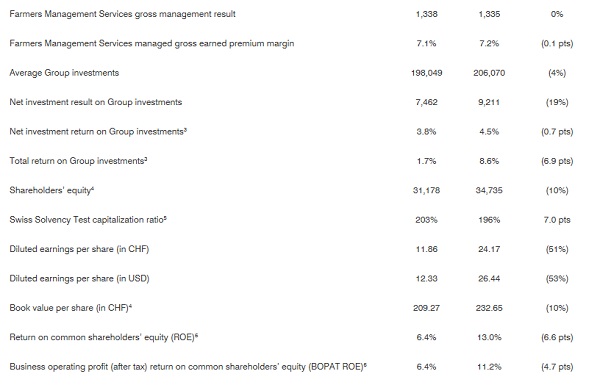

The net investment result on Group investments, which includes net investment income, realized capital gains and losses and impairments, contributed USD 7.5 billion to the Group's total revenues for the year ended December 31, 2015, a net return of 3.8%. The total return on Group investments, which in addition to the net investment result includes changes in unrealized gains/(losses) reported in shareholder's equity on investments classified as 'available-for-sale', was 1.7%, compared with 8.6% in 2014. The decline in in the total return was mainly the result of rising bond yields, widening credit spreads and an overall decline in equity markets in 2015.

Subject to shareholder approval at the AGM of March 30, 2016, the proposed 2015 dividend will be paid from Zurich Insurance Group Ltd’s capital contribution reserves.

1.Parentheses around numbers represent an adverse variance.

2.Total Group business volumes comprises gross written premiums, policy fees, insurance deposits and management fees generated within General Insurance, Global Life and Farmers.

3. As of December 31, 2015 and December 31, 2014, respectively.

4. Shareholders’ equity used to determine ROE and BOPAT ROE is adjusted for unrealized gains/(losses) on available-for-sale investments and cash flow hedges.

5. Details of the principles for calculating new business are included in the embedded value report available on-line at www.zurich.com. New business value and new business margin are calculated after the effect of non-controlling interests whereas APE is presented before non-controlling interests.

6. Zurich Insurance Group has no ownership interest in the Farmers Exchanges. Farmers Group, Inc., a wholly owned subsidiary of the Group, provides administrative and management services to the Farmers Exchanges as its attorney-in-fact and receives fees for its services.

Financial highlights (unaudited)

The following table presents the summarized consolidated results of the Group for the year ended December 31, 2015 and 2014, and the financial position as of December 31, 2015 and December 31, 2014, respectively. All amounts are shown in U.S. dollars and rounded to the nearest million unless otherwise stated, with the consequence that the rounded amounts may not add to the rounded total in all cases. All ratios and variances are calculated using the underlying amounts rather than the rounded amounts. This document should be read in conjunction with the Annual Report 2015 for the Zurich Insurance Group and with its Consolidated financial statements 2015. In addition to the figures stated in accordance with International Financial Reporting Standards (IFRS), the Group uses business operating profit (BOP), new business measures and other performance indicators to enhance the understanding of its results. Details of these additional measures are set out in the separately published Glossary. These should be viewed as complementary to, and not as substitutes for the IFRS figures.

1. Parentheses around numbers represent an adverse variance.

2. Details of the principles for calculating new business are included in the embedded value report available on-line at www.zurich.com. New business value and new business margin are calculated after the effect of non-controlling interests, whereas APE is presented before non-controlling interests.

3. Calculated on average Group investments.

4. As of December 31, 2015 and December 31, 2014, respectively.

5. Ratios as of January 1, 2015 and July 1, 2015, respectively. The Swiss Solvency Test (SST) ratio is calculated based on the Group's internal model, which is subject to the review and approval of the Group's regulator, the Swiss Financial Market Supervisory Authority (FINMA). The ratio is filed with FINMA at the full year and is subject to its approval. The July 1, 2015 ratio is calculated excluding the macro equity hedge, for more details please refer to the Risk review section in the Annual Report 2015.

6. Shareholders’ equity used to determine ROE and BOPAT ROE is adjusted for unrealized gains/(losses) on available-for-sale investments and cash flow hedges.

Further information

The analyst and investor slide presentation will be available from 06.45 CET.

Live media event

There will be a live media event at Zurich’s headquarters starting at 09.00 CET with Chairman and Chief Executive Officer a.i. Tom de Swaan, Chief Financial Officer George Quinn, General Insurance CEO Kristof Terryn and Global Life CEO Gary Shaughnessy. Chief Investment Officer Urban Angehrn will be available to answer questions. Journalists who are unable to attend in person, may dial in using the details provided below.

The presentation will be held in English

The media presentation will be available from 08.30 CET on www.zurich.com.

Q&A session for analysts and investors

There will be a conference call Q&A session for analysts and investors starting at 13.00 CET. Media may listen in. A podcast of this Q&A session will be available from 17.00 CET. Please dial-in to register approximately 10 minutes prior to the start of the respective conference call.

Dial-in numbers

• Europe +41 (0)58 310 50 00

• UK +44 (0)203 059 58 62

• USA +1 (1) 631 570 56 13

Supplemental financial information is available on our website.