Unlocking growth in complex conditions

SA’s major banks delivered strong earnings growth against complex operating conditions, a volatile macroeconomic context and a local economy under strain

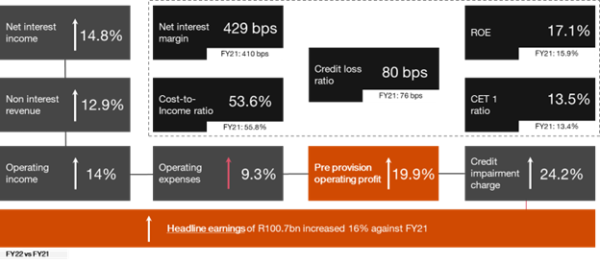

Combined headline earnings growth of 16.1% against FY21 to R100.7bn, combined ROE of 17.1% (FY21: 15.9%), net interest margin of 429 bps (FY21: 410 bps), credit loss ratio of 80 bps (FY21: 76 bps), cost-to-income ratio of 53.6% (FY21: 55.8%), common equity tier ratio of 13.5% (FY21: 13.4%)

2022 tested the resilience of the South African economy, which began with momentum as the disruptive phase of the COVID-19 pandemic eased. After rallying in the third quarter, StatsSA reported that GDP declined by 1.3% in the fourth quarter, elevating recessionary concerns. The relative cover to the South African economy in the first half of 2022 through a commodity price boom and strong terms of trade faded swiftly as severe electricity supply constraints, the aftermath of the KwaZulu-Natal floods and slow progress on structural reforms strained trading conditions and sentiment. Globally, complex geopolitics, lockdowns in China and the Russia/Ukraine conflict combined to exert significant inflationary pressure on the global economy, elevated input costs for most African economies and created choppy financial markets.

Reflecting on the major banks’ results for 2022, Rivaan Roopnarain, PwC Africa Banking and Capital Markets Partner, says: “Against complex trading conditions and a volatile macroeconomic backdrop, South Africa’s major banks delivered strong earnings growth on the back of robust operating performances across all franchises, larger balance sheets and intense focus on translating superior customer experiences into heightened transactional activity.”

Key themes observed from PwC’s Major Banks Analysis include:

- Robust operational momentum across retail, business and corporate banking franchises, strong customer activity, strength and depth of transactional and deposit franchises and the positive endowment effects of an elevated interest rate cycle provided the basis for the major banks’ revenue growth in 2022.

- Measured approaches to credit origination, rigorous monitoring and collections strategies together with relatively improved business and consumer balance sheets in the first half of 2022 facilitated well-managed credit metrics. However, this was partially offset by higher corporate and Ghanaian sovereign exposures. Non-performing loan stock increased largely due to the credit migration effect of new business written in previous periods, while credit coverage levels were maintained at traditionally prudent levels.

- Driven by organic capital supply through higher earnings and optimised capital demand through disciplined credit quality management, capital ratios remained resilient, well above regulatory required levels. As we previously observed, SA’s major banks collectively now have more capital and risk provisions than ever recorded, which helped to shield against economic headwinds that emerged over the second half of 2022.

- A focus on building and deriving value from more diverse revenue generators continued, particularly in the form of insurance, wealth management and related activities. Those banks with notable operations in these areas observed strong operational performances and a growing contribution to overall group earnings.

- Geographic diversity remained central to earnings contributions, with those banks with sizable physical footprints across the continent outside South Africa registering roughly a third of group earnings from these operations. With Africa’s young, mobile and IT-savvy population, economic growth expectations across the continent are forecast to exceed SA’s GDP growth — at least until accelerated progress on structural reforms takes place. Accordingly, some of the major banks will continue to look for opportunities to deploy capital in territories that yield elevated returns.

- Disciplined cost management in a heightened inflationary environment was a central theme across bank management teams, and supported strong operating leverage as combined revenue growth surpassed cost growth. The trend of the changing configuration of the major banks’ cost base that we commented on previously, continued. Driven by their digitally-led focus, efforts to streamline IT architecture, enhance front-end customer experiences and boost productivity, we continue to see deliberate IT expense growth, together with talent spend, in these areas.

- Competition in South African retail and business banking remained intense, amplified by niche lenders with more agile tech stacks and new product offerings. In commenting on their results, the major banks’ management teams have acknowledged this trend, and their determination to bolster their strategic plans while focusing on the significant opportunities that technological and competitive disruption presents.

- Delivering top-tier client experiences particularly in retail transactional and personal banking, and an enhanced ESG focus, remain common themes across the major banks. Each of the major banks have commented on their stated intentions to play a greater role in enabling corporate and business clients to meet their climate obligations. Each of the major banks now have clear commitments to support renewable energy and infrastructure projects and just energy transition efforts. We expect sustainable financing disclosures, alongside broader measures of performance based on emerging ESG practices, will begin to take greater prominence in corporate reporting.

- The risk outlook remains dynamic and evolutionary. While 2022 revealed that traditional financial and economic risks can move quickly, methodologies for their identification and measurement are well established. However, against the backdrop of rapidly evolving financial market digitisation in the form of blockchain technology and asset tokenisation, 2022 also revealed that market shifts represent a generational opportunity to build new growth engines and risk management capabilities that include identification of second- and third-order risks tied to reputational and societal concerns.

Major banks’ results highlights: PwC’s Major Banks Analysis highlights key themes from the combined local currency results of Absa, FirstRand, Nedbank and Standard Bank, and provides reflections from the common strategic themes within the other South African banks.

Costa Natsas, PwC Africa’s Financial Services Leader, says the major banks proficiently maneuvered through difficult operating terrain in the second half of 2022. “Through their consistent focus on helping clients navigate a once-in-a-generation pandemic, refinements to bank strategy in response and intense execution of their strategies, South Africa’s major banks have shown their resilience. They have surpassed the most rigorous stress test since the global financial crisis, while leveraging and embedding lessons learned to position their businesses to efficiently respond to dynamic and complex conditions.”

- Headline earnings: For some of the major banks, headline earnings again reached record levels. Key drivers of earnings growth in this period included a combination of cyclical factors — the positive endowment effect on net interest margins brought about by a high interest rate environment and fair value realisations — and those based on disciplined strategy execution, including sustained efforts in prior periods to ensure front-end customer experiences facilitate seamless and efficient transactional activity.

- Asset growth: Bureau information from the National Credit Regulator for 2022 revealed that the South African consumer exhibited increased credit demand in the period, with the number of credit-active consumers increasing by 227,924 year-on-year in Q3-22. Secured lending portfolios, in particular residential mortgages, continued on the growth trend observed previously. Overall, gross loans and advances grew 8.3%.

- Credit quality: The well-documented theme of judicious credit management continued during 2022, with the combined credit loss ratio (measured as the income statement impairment charge divided by average advances) marginally increasing by 4 bps to 80 bps (FY21: 76 bps). Total non-performing loans increased 9.2%, comprising 4.7% of gross loans and advances (FY21: 4.7%), while expected credit loss provisions against these loans moderated slightly to 44.9% (FY21: 45.8%).

- Costs: Against the context of 6.9% average CPI in SA in 2022, the combined operating expenses of the major banks grew 9.3%. Key contributors to the combined cost base included relatively familiar themes of staff costs and incentive awards amidst a fierce talent retention backdrop, front- and back-office technology related spend, driven also by cloud and cloud-related software investments, and a resurgence in travel and marketing expenses.

- ROE and capital: Having surpassed pre-pandemic levels in the previous reporting period, the combined regulatory capital of the major banks was bolstered further on the back of robust earnings growth and disciplined risk-weighted asset management. The total capital adequacy ratio amounted to 16.2% (FY21: 17.2%) and supported dividend payout ratios in the period. Combined ROE grew 120 bps to 17.1% (FY21: 15.9%).

Francois Prinsloo, PwC Africa’s Banking and Capital Markets Leader, says: “The results of the major banks in this period reflect the intense efforts of management teams to take the pulse of the operating environment, and calibrate their actions accordingly. Driven by underlying customer, lending and operating momentum, the deep focus on embedding digital strategies, channel innovation and enhancing overall customer experiences, helped position our banks to the strong levels of growth their results reveal.”

Outlook: For 2023, the major banks have commented on their expectations for central banks to pause, or decelerate, their recent rate hiking cycles on the back of moderated inflation forecasts relative to that observed in 2022. While the International Monetary Fund estimates global real GDP growth of 2.9% for 2023, concerns exist for the slowdown in developed economies to escalate as the effects of 2022’s high interest rate environment impair household and business incomes and trigger reduced wealth effects. Additionally, the ongoing Russia/Ukraine situation fuels concerns around supply chain bottlenecks, energy constraints and higher production costs.

Meanwhile, sovereign risks across the African continent — including in Ghana, Nigeria, Malawi, Zambia and Mozambique — are expected to remain elevated while those countries with fiscal constraints and/or notable levels of dollar-denominated sovereign debt may continue to face economic headwinds.

In SA, the major banks all consistently shared their reflections that the unprecedented levels of load shedding experienced in 2022 and into 2023, coupled with the slow pace of structural reforms, remains a noose around the South African economy’s growth potential and medium-term growth prospects. On average, the major banks estimate SA’s GDP will grow by a modest 1.3% in 2023.

Despite significant progress by authorities during 2022, in February 2023 the Financial Action Task Force (FATF) greylisted SA. As we have previously commented, the implications of the greylisting are broad, and include increased monitoring by FATF, more onerous reporting requirements by correspondent banks, possible restrictions on correspondent banking relationships and potential pressure on funding costs.

As we look ahead, we see that the financial environment is once again entering a period of volatility — with rates, inflationary concerns and geopolitical instability on the rise. To weather these forces, our global research suggests that banks must accelerate and scale their transformation agendas so that they can address ‘old’ and new challenges simultaneously. Market structures are changing, exposures have become more complex and interconnected, new asset classes are becoming too large to ignore, and non-financial factors such as ESG are now critical business drivers. Our latest global PwC report, Wholesale Banking 2025 and Beyond, suggests that banks must manage the tension between day-to-day operations alongside a programme of sustainable change as a range of market forces — including technological disruption, competition from non-traditional players, geopolitical shifts, sharp inflationary spikes and pressure on global supply chains — combine to present new challenges and far-reaching implications to banks.

The major banks’ FY22 results, and the drivers behind them, suggest that our banks are acutely aware of these challenges, how to navigate them and incorporate them into the determination and refinement of overall bank strategy. We expect this dynamic process of strategic planning, with internal and external digitalisation and customer centricity at its heart, to continue.