SA Banks navigated the coronavirus crisis commendably thus far

Jeremy Gorven, Senior Analyst at International Family Office Firm Stonehage Fleming

Seven months into the coronavirus crisis, a health check on South Africa’s financial system reveals that its banks have coped relatively well under stress, recovering to high levels of liquidity and capital adequacy. The system has remained profitable amidst a significant rise in impairments, and efficiency has improved in a lower revenue environment.

Demonstrating robustness

“Our banks have shown robustness,” says Jeremy Gorven, Senior Analyst at international family office firm Stonehage Fleming. Liquidity, which is crucial for maintaining confidence in the banking system, is strong.” The liquidity coverage ratio has recovered to 147%, well above the required level of 80%.

“The healthy return on equity produced by South African banks prior to the crisis enabled them to absorb the shock increase in impairments whilst remaining profitable. This undoubtedly saved jobs,” he said.

Encouragingly, the growth in credit impairments seems to have slowed and then stopped as impairments plateaued between July and September 2020.

Bank profitability has declined by 46% year on year to an 8.2% return on equity due to increased impairments, lower interest income and lower transactional revenue. As impairments have flattened out and banks have begun to improve their cost efficiency, the decline in returns has slowed.

“All systemically important banks, which make up 92% of system assets, recorded a profit for the half year ended June/August 2020. The reserve bank has however always been more cautious on smaller banks, for which there is less disclosure,” said Gorven.

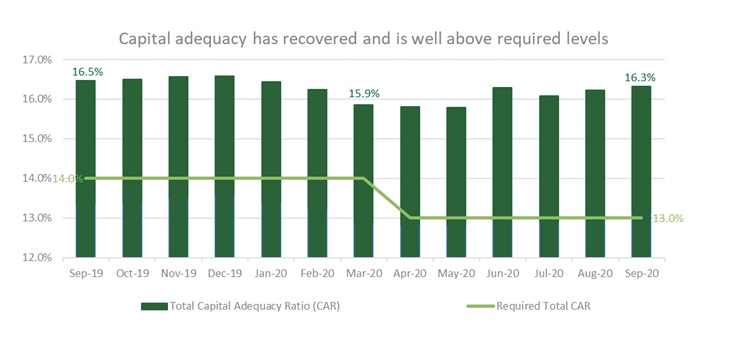

As banks remain profitable on aggregate and are retaining capital over paying dividends, the capital adequacy of banks has recovered to 16.3%, well above the required levels.

Source: South African Reserve Bank – Prudential Authority, November 2020

Outlook for continued economic recovery

The SARB states that the “SA economy is picking up fast from a deep Q2 trough” with some indicators already back to pre-COVID levels.

Lower interest rates and lower inflation are helping the economy adjust and helping the affordability of credit. Reduced economic restrictions combined with the low rate environment are supporting growing demand for credit. However, the recovery is being impeded by fiscal imbalances and electricity shortages.

“A healthy banking system is a key enabler for economic recovery and growth. Amidst an improved capital and liquidity position, South African banks are positioned to support a recovery; particularly should there be meaningful progress on fiscal consolidation and structural reform. In relation to our BRICS peers, South Africa’s bank capital ratios compare favourably.”

Gorven said the announcement of two COVID-19 vaccine candidates with 90+% effectiveness is positive for bank return outlooks from the perspective of higher yields on assets, greater transactional activity in the economy, lower impairments and a more efficient cost base. Prior to an implementation of a vaccine or vaccines, the possibility of future tightening of restrictions on economic activity remains. As can be seen from the adequate level of capital, banks have rebuilt a buffer against future impairment shocks.

“Although impairments may remain high for some time, bank returns may begin to stabilise and improve amidst increasing activity, improved efficiency and an impairment peak. For the higher return banks including Capitec, Standard Bank and First Rand, this might enable the recommencement of dividend payments sooner rather than later.”