Bank confidence remains weak, led by falling investment bank sentiment

Andrew Bates, Financial Services sector leader at EY Africa.

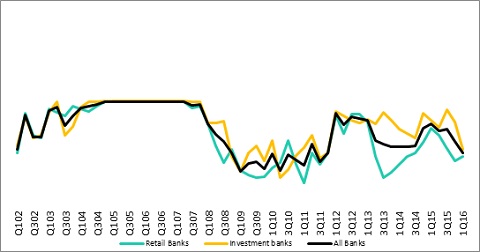

A survey released by EY today indicates that banking confidence remained weak in the first quarter of 2016, with investment banking confidence falling sharply, but remaining nevertheless above retail banking levels. Investment banking confidence fell a strong 27 index points.

Overall banking confidence weakened on the back of the softer investment bank sentiment, from 61 index points in the fourth quarter of 2015, to 50 in the first quarter, well below the long term average level of 72 index points, and reflecting the weak prevailing business conditions.

Bank confidence levels

This is the 57th quarterly survey measuring confidence in the banking industry, and the research is conducted by the Bureau for Economic Research in Stellenbosch.

Comments Andrew Bates, Financial Services sector leader at EY Africa, “The weaker bank confidence is a reflection of the weak and declining economic fundamentals that South Africa continues facing. Confidence levels are down across most, if not all industries, and bank earnings are largely concentrated in South Africa, despite growing diversification efforts into the rest of Africa.”

Bates adds, “Bank confidence has remained weak (below-average) over the last four years, bar a very brief spell towards the end of 2014. This weaker sentiment really reflects the slow growth environment. We have seen GDP growth slow from the 3% range in 2013 to its current 0.8% expected in 2016. Each of the banks that have recently reported results, mentioned the macro environment as a fundamental concern.”

He further adds that, “The weaker investment bank confidence is in line with sharply contracting business volumes. There was a particularly sharp fall in volumes across the board during the first quarter, with stockbroking and private equity most visibly impacted.”

The survey results also show that investment bank confidence was in line with weak profits growth. Profits growth slowed sharply during the first quarter, to its lowest level in at least two years.

Bates adds, “There are a number of factors driving these slower corporate bank earnings. Investor confidence remains very weak, and corporate entities are inclined to hold back on investing in such a climate. As a result, corporate credit demand remains weak by historical levels. There is thus much slower appetite for investment banking activities, as a result of which we saw those activity levels falling off sharply, impacting fee income as a result. The weak investor sentiment also hurt investment income, which shrunk during the quarter.”

Retail banks, by contrast, have a more stable market environment albeit a very low growth one. Bates comments that, “The recent financial reporting cycle showed that retail bank earnings grew more rapidly through 2015 than corporate banking earnings did, despite the weak economic fundamentals in the lower income segments.”

Other survey findings include:

Investment banking

• A slight easing in the pace of credit loss growth.

• A bias towards stricter credit policy application for the first time in two years.

• Slowing expenses growth, although these remain high by historical levels.

• Resumption of headcount reduction, after a respite in 4Q15.

Retail banking

• Continued income growth slowing, being marginally positive in the first quarter, and with an expectation that it will contract in the second quarter.

• Considerably softer cost rises, in line with weaker revenue growth.

• A small uptick in credit losses, although these remain within manageable levels overall.

• Continued tightening in credit standards, although at a somewhat gentler pace than the previous few quarters.

• Profits continue to grow at moderate levels.

Bates also believes the rising credit impairment and tighter lending criteria are likely to increase in intensity through the rest of 2016. “Whilst retail banks experienced an earlier uptick in credit impairments, we have more recently seen that corporate and investment banks are experiencing a similar increase, although off a much lower base. In the recent reporting cycle, the credit impairment ratio was little changed through 2015, but with recent interest rate increases and squeezed disposable income, coupled with falling corporate profits growth, banks expect to see impairments rising over the next few quarters.”

He concludes by saying, “2016 will likely prove to be another tough year for the banking sector, although it will be equally difficult across most sectors. One potential silver lining is the recent stronger emerging market sentiment that has been evident since the middle of February or so. This could provide some uplift – particularly for investment banks, who will benefit from stronger mining and manufacturing activity. They will also be well placed for advisory work in the African growth space.”