Bank confidence improves despite weak profits

Andy Bates, Financial Services Africa leader at EY.

A survey released by EY today indicates that banking confidence rose in the second quarter of 2016, but remains below long-term average levels.

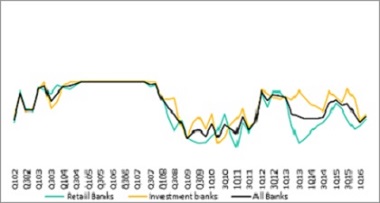

Overall banking confidence rose despite shrinking investment bank profits, rising from 50 to 58 index points in the second quarter, somewhat below the long term average level of 72 index points.

Bank confidence levels 2002 – 2Q2016

This is the 58th quarterly survey measuring confidence in the banking industry, and the research is conducted by the Bureau for Economic Research in Stellenbosch.

Comments Andy Bates, Financial Services Africa leader at EY, “Weak bank confidence has been evident since the middle of 2013. If we look at typical confidence levels, there is undoubtedly a pre and post global financial crisis (GFC) era distinction.”

Bates adds, “Local banking confidence averaged 97 index points in the five years building up to the crisis. Thereafter, confidence has averaged 58 index points.”

He points out that this is not dissimilar to other countries, where there is a ‘new-normal’ that has emerged. What that means is that returns, profits, and lending growth have all adjusted to increased regulatory scrutiny, with greater compliance requirements and supervision from the authorities, collectively forcing banks to take a more internal focus. Banks in a post GFC world are also required to hold larger capital holdings, and this has had a direct impact on bottom line profits and shareholder returns. And of course, growth across much of the globe has slowed.

In the case of South Africa, the cycle was slightly different, but interestingly, driven primarily by under-performing mortgages. This followed local home-loan lending growth of 25% per annum in the years leading up to the GFC. These growth rates proved problematic, and each major bank faced significant losses in its home-loan portfolios at some point.

More recently, weak bank confidence is driven by sustained low economic growth. Credit demand has been growing in single digit territory, and the latest data indicates that growth slowed even more noticeably in the second quarter. Says Bates, “The latest loan growth data indicates that bank lending to the private sector is barely keeping pace with inflation. In other words, in real terms, lending is at best flat. This provides a major reason for overall bank confidence trailing long term average levels.”

The survey results also show that retail and investment banking confidence are far closer than they have historically been. Bates adds, “Over the last few years, retail banks have typically been far less confident than their investment bank peers. This has changed over the last two quarters, and is indicative of a very weak economy, where both the corporate and household sectors are under pressure.”

Other survey findings include:

Investment banking

• Continued weak business volumes, with all but one business line reporting shrinking volumes;

• Pressure across fee and investment income;

• Net interest income is lower, but in line with averages over the last two years; and

• Sharply shrinking net profits during the quarter, to the lowest level in over three years.

Retail banking

• Sustained weak income growth, driven by flat interest revenue and shrinking fee income;

• A sharp slow-down in net profits – to the lowest levels in at least three years;

• Credit losses continue to rise, in line with first quarter levels; and

• Continued tightening in credit standards, in line with the previous quarter.

Bates concludes by saying that the revival of bank confidence will depend on renewed economic growth. He believes there are some grounds for optimism. “Recently we have seen enhanced business and government cooperation, which could see more pragmatic policies adopted. In addition, emerging market currencies are holding steady, and that will provide relief to households, as lower import prices strengthen disposable income. So on both the retail and corporate fronts, we should see improving prospects in the second half of 2016. This will benefit banks, as it will industry more broadly.”