2015 Africa’s bank profits weaken on constrained lending

Andy Bates, Financial Services Africa Leader at EY.

An overview of the banking performance across Africa’s largest banking markets released by EY today, indicates that banking profits shrunk in 2015, with South Africa’s banks showing stronger resilience to the economic downturn.

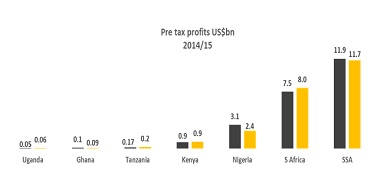

The overview finds that banking profits contracted from $11.9bn in 2014, to $11.7bn in 2015. The results are analysed on a constant currency basis, to ensure that exchange rate fluctuations do not impact the results.

Source: Banks annual reports, EY analysis

The review of African banks covers the largest 26 banks in some of the largest banking markets across Africa.* The markets covered are South Africa, Nigeria, Kenya, Tanzania, Uganda and Ghana.

Andy Bates, Financial Services Africa Leader at EY says, “The slow-down would be attributable to South Africa’s slow growth but this is not the case. He adds, “South Africa’s banking profits were robust in 2015, despite the weak local growth. Those banks with sizeable African operations did particularly well, despite the slower growth across the rest of the continent.”

The review shows that pre-tax profits in Nigeria’s banking sector fell a sizeable 29% last year, whilst Kenya’s banking profits were only marginally positive (+4.4%), albeit following a number of years of strong double-digit growth. The overall 1.9% contraction in profits across the continent follows a robust 2014, when profits rose 15% in constant currency terms.

Overall, Tanzania’s banks fared strongest across a broad range of financial metrics in 2015. The country’s banks saw the fastest asset growth, the strongest profits growth, and was the only country whose banks reported improving efficiencies. In addition, Tanzanian banks benefitted from slowing impairments. Bates points out that East Africa was most immune to commodity cycle downswing that is currently hurting most commodity exporters across Africa. “Tanzania’s growth has held up remarkably well, with final GDP growth at over 7%. This makes the country one of the fastest growing globally, and puts the East African Community** on track to become a $200bn market by 2025.”

The analysis focuses on the drivers of earnings across the key markets. Amongst the high level findings are:

• Nigeria’s weaker earnings were attributable to significantly slower asset growth, coupled with sharply rising impairments.

• Kenya’s profits slowed to low single digit territory, despite asset growth remaining well in double digits(+14.1%).

• South Africa’s higher profits were somewhat obscured by a rebound at one bank, rather than being broad based. Whilst overall profits rose 16.6%, most banks reported growth of high single digits or at best, low double digits.

Bates comments that, “If there was one single issue faced by banks across the continent, that was weakening economic growth and the impact it had on bank lending and impairments. This was particularly evident in Nigeria, where bank assets grew a marginal 2.1% during the year, by far its slowest pace since the banking crisis the country endured in 2011. At the same time, the country’s credit impairment ratio for the largest banks rose a considerable 120 basis points.”

Not only did banks face weakening asset growth coupled with rising impairments, they also faced other headwinds. Margin pressure was visible – particularly in Kenya. However, even with downward pressure on margins, the banking sector remained strong in East Africa, with Kenya and Tanzania enjoying margins of 9.8% and 10.5% respectively, amongst the highest on the continent.

In addition to weakening margins (in four of the six markets covered referred to above), banks also had to manage continuing cost pressures. Says Bates, “It is easier said than done to contain cost growth when income starts slowing. Typically banks have long term programs, both in terms of expansion plans and in back-office platform investments. These are not easily discarded, as the commitments are often made well ahead of the time that the expenditure is actually incurred.”

As a result, efficiency ratios were higher across five of the six markets covered, with Tanzania’s banks alone bucking the trend. South Africa saw only a marginal 10bps rise in the industry efficiency ratio. The survey finds the largest pressures were in Ghana*** Kenya, and Nigeria, with all three markets showing a 90 bps increase or more.

Bates concludes that although 2015 proved to be a difficult trading environment for the banking sector, 2016 is unlikely to be any easier. “We have seen the World Bank and IMF, amongst others, trim their growth forecasts for the year ahead. SSA overall will likely grow at around the 3% level, somewhat below its more recent performances of 5%+. The oil exporters particularly remain pressured for now. We expect regulatory, consolidation and ownership issues to permeate the sector through the remainder of this year and into the next few years ahead. Having said that, the medium term prospects for banks remain very exciting. The need for infrastructure spend remains critical and banks that fund these needs are well positioned for the long term. In addition, as Africa’s economies mature, so they become more formal and that brings a larger number of people into the financial services matter. We remain very optimistic on longer-term growth prospects.”